Get a call back!!

Get a call back!!

1800-12000-0055

A Health Insurance plan covers the costs that may arise due to any unforeseen hospitalization/ medical procedures. Health insurance covers the medical expenses for illnesses, injuries, and other medical conditions. In general, a health insurance plan offers a financial guard against financial drainage on several diseases. With health insurance, you don’t need to worry about treatment expenses. and treatment

| Insurance Companies | Health Plans | Sum Insured (Min/Max) | Pre- Existing Diseases | Co-Payment | Pre/Post Hospitalization | No Claim Bonus |

|---|---|---|---|---|---|---|

| Care Health Insurance Co. | Care Plan | 3 Lakh/75 Lakh | Covered after 4 years | Applicable | 30/60 days | Max up to 150% of SI |

| Star Health Insurance Co. | Family Health Optima Insurance Plan | 3 Lakh/25 Lakh | Covered after 4 years | Applicable | 60/90 days | Max up to 35% of SI |

| Bajaj Allianz General Insurance Co. | Bajaj Allianz Health Guard | 1.5 Lakh/10 Lakh | Covered after 4 years | Applicable | 60/90 days | Max up to 50% of SI |

| Universal Sompo General Insurance Co. | Complete Health Care Insurance | 1 Lakh/ 10 Lakh | Covered after 3 years | Applicable | 30/60 days | Max up to 50% of SI |

| ManipalCigna Health Insurance Co. | ManipalCigna ProHealth Plus Plan | 2.5 Lakh/10 Lakh | Covered after 4 years | Applicable | 60/90 days | Max up to 100% of SI |

| Future Generali General Insurance Co. | Future Health Suraksha Plan | 50,000/10 Lakh | Covered after 4 years | Applicable | 60/90 days | Max up to 50% of SI |

| HDFC Ergo General Insurance Co. | Health Suraksha | 3 Lakh/75 Lakh | Covered after 3 years | Applicable | 60/180 days | Max up to 100% of SI |

| ICICI Lombard General Insurance Co. | Complete Health Insurance | 3 Lakh/50 Lakh | Covered after 4 years | Applicable | 30/60 days | Max up to 50% of SI |

| HDFC Ergo General Insurance Co. | Optima Restore Individual | 3 Lakh/50 Lakh | Covered after 3 years | Not applicable | 60/180 days | Max up to 100% of SI |

| Niva Bupa Health Insurance Co. | Health Companion Health Insurance | 2 Lakh/50 Lakh | Covered after 4 years | Applicable | 30/60 days | Max up to 100% of SI |

| Star Health Insurance Co. | Star Comprehensive Insurance Policy | 5 Lakh/25 Lakh | Covered after 4 years | Applicable | 30/60 days | Max up to 100% of SI |

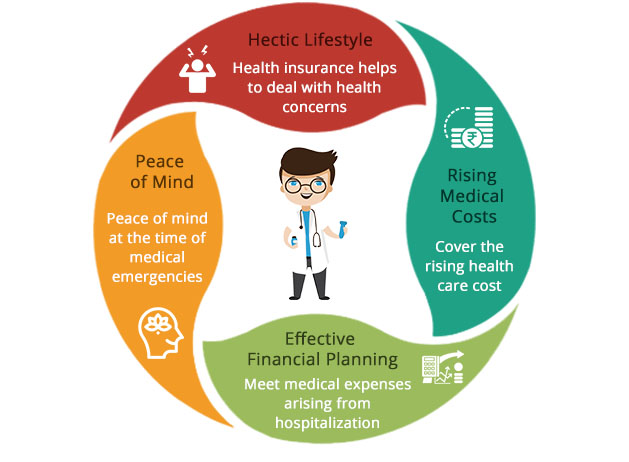

Here are some top reasons why you should buy a Health Insurance Policy.

Nowadays, people are busy in their day-to-day life, and typically, they don’t have time to look after their health concerns. The hectic lifestyle makes the body suffer from high-stress levels that can lead to serious health issues. In case you need medical treatment, you should be covered by health insurance.

The medical treatments are becoming unbelievably expensive. 75% of Indian households are paying medical bills out of their pocket. Innovation and development in the medical arena have resulted in the cure for most life-threatening illnesses. Treatment for such critical diseases carries enormous medical costs and thus is not affordable to ordinary people. Treatment in private hospitals will cost you to the extent of bringing a quake in your financial stability.

Anybody may fall ill, and several medical treatments, especially a critical illness, can obstruct you from achieving your financial goals. If you are not covered by medical insurance, you need to pay the enormous medical bills with money you kept for meeting other financial objectives like buying a car or a new home. If you are the only income-earning family member, it becomes imperative to get yourself health insurance at the earliest.

By buying a health insurance policy, you will get coverage against hospitalization expenses for you & your family. With the health cover, you don’t need to worry about medical expenses, and it ensures peace of mind during medical emergencies.

Choose the best Health Insurance Policy in India and lessen your financial risks from unforeseen health problems. There are different types of health plans you can choose from depending on you and your family's health needs.

This kind of health insurance plan is designed to provide medical cover for an individual. It is a preferred health insurance plan when you are unmarried or the only earning member of your family. This health insurance provides cover against in-patient hospitalization expenses, pre & post-hospitalization expenses, and daycare procedures. You only need to ensure that you are not under-covered and opt for the right insurance cover under an individual health policy. Such policies are also known as Mediclaim Policy.

If you want to cover your entire family's medical expenses, you can go for a Family Floater Health Plan. Under this Health Insurance Plan, your whole family, including spouse, parents, kids, and some plans also allow parents-in-law who can be included as insureds under one policy and claim against hospitalization or medical benefits as per policy contract. At one time, more than one member of your family can also avail of the advantages of this health insurance plan subject to the maximum limit. The total health cover or Sum Assured can be shared between the multiple insureds within a single policy year.

As you grow older, there are more chances of getting sick. In case you go through medical treatment, you have to pay substantial medical bills from your pocket, which is quite painful, especially when you don't have a regular source of income. It is thus better to choose a Senior Citizen Health Insurance Plan to put a cover on your finances. You can choose an umbrella plan which includes you and your spouse (if you fall in the senior citizen category), or you can buy individual senior citizen health plans. These health plans cover the medical needs of senior citizens.

Critical illness is a health-related medical condition of a severe nature. A Critical Illness insurance plan guards you against the financial expenses in diagnosing acute diseases such as cancer, heart attack, kidney failure, etc. The range of critical illnesses covered and the payout may vary from one plan to another. Critical illness insurance provides a lump-sum payment in case the policyholder is diagnosed with the critical illnesses mentioned in the contract. A critical illness plan can also be taken as an add-on benefit to your base health plan.

A Personal Accident Plan provides you with cover against accidental death or injury resulting in permanent total/partial disablement. Severe accidental injuries affect the earnings of the person. When it comes to securing the future of the family, this plan is quite essential for the sole earning member of the family. This plan pays the sum assured to the insured (in the event of disability due to an accident) or nominee (in the case of death). Some Personal Accident insurance policies also cover Medical Expenses arising out of the accident. The Personal Accident Plan can also be taken as an add-on benefit to your base health plan.

Under this plan, medical expenses pertaining to maternity are covered. It covers the cost of maternity expenses which are incurred during childbirth. Insurers put some waiting period to avail this cover. Some insurers include maternity benefits inbuilt under their primary health plan also.

A group health insurance policy is a type of insurance plan which provides health care insurance coverage to a group of people, who are usually an employee of a common company, professionals in a common group, or members of a cooperative society. For most salaried people, group health insurance comes as one of the most beneficial perks, which is offered by an employer. The group health insurance policy helps a company to mitigate the risk faced by their employees and increases employee satisfaction also. A group health insurance policy, is a policy issued for one year, which needs to be renewed annually to continue coverage.

Following are the key determinants for computing the premium amount for your chosen Health Insurance Plan or Mediclaim Policy.

The sum assured or health cover you opt for determines the premium amount for your health plan. You should select the adequate sum assured, keeping medical inflation in mind so that you get enough coverage for your medical conditions. A higher sum assured attracts a higher premium.

If you buy a health plan at a young age (age bracket of 18-25 years), you will be charged lesser premium rates than those aged 40+ years. People at a younger age are less likely to face critical health issues, and thus, your insurer will charge a lesser premium.

The individual health plan has a lower premium than the family floater health plan. The number of insured covered under a single policy results in to increase in premium. Under a Family Floater Policy, the insurance company provides cover for each member of your family who is insured under the health plan and so, the premium is also relatively higher than individual health policy.

If you have any pre-existing health condition, your insurance company will charge a premium at a higher rate. It is recommended to inform them about your pre-existing condition to the insurer while buying the health plan, so you can easily get the claim afterward.

Best Health Insurance Plans in India consider personal health status before giving a health insurance policy. Personal health is a vital determinant that decides the cost of the premium. If an individual is healthy, then it reduces his chances of getting hospitalized, whereas if a person has any genetic disease, the health insurance premium will be high, or the disease would be omitted from the coverage, basis the terms and conditions laid by the insurance company. Also, if you are in the habit of taking drugs, chewing tobacco, or smoking, you are charged with increased premium rates. These unhealthy habits directly put you at a high health risk and thus affect the premium rate.

Getting a claim-free year may result to a discount on the premium rates on your renewal premium or an increase in the sum assured. No claim bonus you earn under your health plan may reduce your premium amount in the subsequent years.

Here are some essential tips that you should consider while buying the Best Health Insurance Policy in India.

Choose a Need-Based Plan: It is important to purchase a health insurance plan wisely. You should get a health plan that caters to all your medical needs, considering the growing medical costs. If you have a family with multiple dependents, opt for Family Floater Plans, which will take care of the health-related costs for the entire family. Also, if you have parents aged above 60, it's prudent to buy them separate individual health plans as including them under a floater policy will result in the usage of maximum sum assured by them only as the age advances people are more prone to diseases due to age factor.

Choose the Right Sum Assured: When buying a plan, apart from understanding its benefits, you also need to select the sum assured (health cover) that can easily cover all your or your family's health treatment expenses. If you are under-covered, you need to pay bills from your pocket, and if over-covered, you need to pay high premiums to get a health cover that you don't require at the current moment. So, be prudent in choosing the sum assured amount.

Go for Lifetime Renewability Health Plan: Some insurers may deny the renewal of your health plan, considering your deteriorating health condition. It is, thus, recommended to go for health plans that offer Lifetime Reliability. With lifetime renewability, you can always cover the health risks irrespective of age and health condition.

Opt for Top-up & Super Top-up: To broaden your health cover, Top-up and Super top-up health covers help you to cover the medical expenses in case the sum assured of your existing health plan exhausts. Rather than buying a new health plan with extended coverage, it is more prudent to go with the top-up /super top-up cover. It is more economical and provides a comprehensive health cover over and above your primary health coverage.

Make a Well-Informed Decision: It’s wise to read the policy document carefully and understand your policy wordings. Before buying a policy, you should know about the benefits and exclusions it offers so that you can make the right decision with the right health plan.

Check Claims Efficiency: It is important to study the claim settlement ratio and turn around the time of settling the claim by the insurance company before buying the health policy. Also, it's imperative to check the efficiency of the Third Party Administrator (TPA) involved. For medical emergencies, the need of the hour is immediate financial support from the insurance company. Choose the insurance company with a higher claim settlement ratio and the fastest claim settlement turnaround time.

Buy Online: Online buying will enable you to compare the health plans or mediclaim policies from multiple insurers to get the best health insurance plan. Comparing plans online will help you understand the benefits provided under the various plans available on the market and you can take an informed buying decision by choosing the best fit.

Best Health Insurance in India offers additional benefits or Riders along with the base policy. Riders are additional benefits attached to your base policy which will offer you boosted benefits apart from your base policy. Add-on covers attached to your health insurance policy help you enhance the protection level. Listed below are the options:

Critical Illness refers to illness, disease, or sickness which even after the treatment, drastically affects the lifestyle of the patient. For example, Cancer, even after the treatment, needs extreme care and may not make an individual’s life as normal as he/she was before. With Critical Illness add-on the cover, the insured is provided with an immediate fixed amount plus the rider cover expenses incurred during the medical procedure as well. By having critical illness covered, you are covered for a wide range of critical illnesses. Critical Illness can also be taken as a standalone policy. Many insurers have separate Critical Illness plans under their health portfolio.

Hospital cash rider provides for the daily cash that you may need for compensating the medical expenses during the stay in the hospital. Typically, you can claim benefits an amount depending on the nature of your stay. You can also claim a higher payout in case you are admitted to ICU. You will be eligible for the rider payout in case you are hospitalized for a minimum of 24 hours.

This add-on cover enables you to enjoy higher sub-limits for room rent in case of hospitalization. A basic health plan typically provides a defined sub-limit to the room rent. With the help of a room rent waiver cover, you can choose an improved room for your hospitalization beyond your basic cover with this rider.

Many insurers have this as an inbuilt rider in their health plans. With this add-on cover, you are covered against the risks that may arise due to the total or partial disablement or death caused by accidents. Personal accident plans are typically offered as a separate insurance cover by paying an additional premium. A personal accident cover is of great help in the event of medical emergencies caused due to the accidents, and this add-on cover provides the separate sum assured apart from your base sum assured. The Personal Accident Plan can also be taken as a stand-alone policy. Many insurers have separate Personal Accident Plans under their health portfolio.

A top-up health policy provides additional coverage to those who have a running health plan. This plan covers the medical expenses that may arise due to an illness/injury over and above the limit of the actual cover. A top-up health plan works by ‘single incidence hospitalization’, however, a super top-up plan looks at the aggregate claim. A super top-up health plan puts together several incidences of hospitalization to cover the medical bills. It covers a total/aggregate of the medical bills in a year, not just the single instance of hospitalization.

(Note: The rider benefit, conditions, and eligibility criteria may vary from insurer to insurer.)

Get QuotesHealth Insurance Portability refers to the right conferred to a health insurance policyholder to switch from one insurer to another without losing the credit gained with respect to the waiting period for a preexisting condition and other time-bound exclusions. IRDAI (Insurance Regulator) had issued guidelines on the portability of health insurance policies. Portability in health insurance has come into force w.e.f 1st October 2011. The health insurance policyholders thereby have the right to buy a policy from another insurance company of their choice. The portability also applies when you switch from one plan to another with the same insurer. Porting of policy is possible only at the time of renewal. You can carry forward the credit given by the previous insurer, such as the waiting period for Preexisting conditions and other time-bound exclusions. You can port your health policy to any general insurer or specialized health insurer. Under this provision, your new insurer is bound to insure you at least up to the sum assured as mentioned under the previous policy.

Following are the conditions/exclusions that are not included in your Health Plan.

• Pre-existing conditions: Any illness that had symptoms or received medical treatment during three months after commencement of the first policy.

• First 30 days: You can’t claim for the first 30 days from the commencement of the health policy. Accident injury claims, however, don’t require a waiting period.

• The first year of cover: During the first year of your policy, some specific illnesses are not covered include Cataract, Hydrocele, Hysterectomy, Fistula in the anus, Benign prostatic hypertrophy, Sinusitis, and Congenital Internal diseases.

• Cost of contact lenses, hearing aids, and specs.

• Convalescence, congenital external defects, the use of intoxicating drugs/alcohol, intentional self-injury, general debility, expenses for diagnostic tests related to the disease for which the insured has not been hospitalized.

• Pregnancy or childbirth-related treatments.

• Naturopathy treatment.

• Dental treatment/surgery.

(Exclusions may differ from one insurer to another and plan to plan.)

Read the do’s and don’ts related to your Health Plan.

| Do’s | Don’ts |

| Fill the proposal form carefully (online/offline) and provide the right information about the people to be covered under the policy. | Let your agent fill the proposal form on your behalf. |

| Disclose details regarding all pre-existing conditions of each person covered under the policy insured. | Provide any false information while filling the proposal form. It may affect the claim payment at a later stage. |

| For your future reference, you may keep one copy of the proposal form with you. | Hide the material facts or pre-existing conditions of the insured/insured’s. |

| Take out time and read through the policy document, and if you are not satisfied with the policy terms, you may cancel the policy within 15 days free look period, starting from the date of the policy issuance. | Sign the proposal form without reading the policy terms and conditions. |

| Do’s | Don’ts |

| Renew the policy on or before the due date online or by visiting one of the registered offices of the insurance company. | Renew after the due date of the policy renewal. |

| Prior to requesting to enhance the sum insured on the policy renewal, you may read through the sum insured enhancement conditions mentioned in the policy document. | Forget to renew the policy. (The lifetime renewability feature is available only with those policies, which have been renewed without any failure.) |

| You should inform your insurer regarding any change in the risk profile of the insured/insured covered under the plan. | Delay informing the insurer of any change in the risk profile of the insured. |

Ans: Some of the best health insurance companies include Aditya Birla Health, Niva Bupa, Care Health, Star Health, SBI General, Manipal Cigna, IFFCO Tokio, and Tata AIG health insurance. You can select the best health insurance company based on the incurred claims ratio, illnesses coverage, co-payment, waiting period, etc.

Ans: By buying health insurance, you will be covered for the costs incurred due to hospitalization or undergoing a medical procedure. It provides the financial cover against the medical expenses incurred on the treatment of any disease or illness.

Ans: When it comes to buying health insurance cover, you need to assess your present health conditions and pick a health policy to ensure your health care needs are properly fulfilled. With a health policy, you will get the complete cover for all your health-related expenses. It is advisable to buy a health policy at a young age, so you will get cover at a reasonable premium.

Ans: In the event of hospitalization due to an illness or injury, you can make a claim with your insurance company to cover your medical bills. While making a claim, you should also assess No Claim Bonus amount you are eligible for not making a claim and then check whether you should claim for hospital bills.

Ans: It refers to the bonus amount that gets accumulated to the sum insured amount for every claim-free policy year. In other words, your sum insured increases with no claim bonus every year without paying any additional premium.

Ans: To buy an individual health insurance policy, you need to be at least 18 years old and the policy comes with the feature of lifetime renewability. While buying a health cover, you need to assess the policy features, coverage and cost.

Ans: Health is wealth. You need to properly take care of your health and for this, it’s wise to buy health insurance for you & your family. It will ensure to get the financial coverage for your health care expenses. You can simply compare health insurance plans from different insurers and pick the right one for you.

Ans: If you are seeking to get coverage for maternity expenses, you need to get the benefit as a rider cover or you can opt maternity cover as a standalone health insurance plan. You need to assess the maternity cover you are looking for and then pick a health plan accordingly.

Ans: When you are looking to buy health insurance, the cost involved will vary depending on health conditions, pre-existing illness, age, lifestyle habits, etc. The cost aspect also varies from insurer to insurer, so you should assess the cost involved and buy the right plan for your health care needs.

Ans: After buying health insurance, if you found that it does not fulfill your health care needs you have the option to cancel your health policy within the free look period as specified under the policy. Upon cancelling the policy, the company will refund the premium after deducting the cost incurred in providing health coverage such as underwriting costs, cost of medical test, taxes, etc.

Ans: A medical condition, illness or injury that exists within three months of the issuance of the health insurance policy. Some examples of pre-existing conditions/diseases include cancer, diabetes, sleep apnea, etc.

Ans: A waiting period is a period of time specified which must pass before the specific health illnesses or conditions will be covered.

Ans: The list of treatments that are generally not covered in a health insurance policy is specified as follows. Self-inflicted injury Alcohol or drug use Treatment of AIDS Pregnancy-related complications Dental treatment Cost of spectacles or contact lenses Cosmetic surgery Treatment done outside India, etc.