Get a call back!!

Get a call back!!

1800-12000-0055

An Endowment Plan is a mix of both insurance and investment. It is a life insurance policy that provides the life cover to the insured by charging mortality cost and provide a return on investment through investing the remainder portion of the premium.The policy offers both death and maturity benefits (whichever happens earlier).Endowment policy helps you to accumulate adequate corpus along with providing financial protection in case of any unfortunate event to accomplish the financial goals in your life like child's education, marriage, post-retirement expenses, etc.

Get QuotesFollowing are some of the top reasons to buy an Endowment Plan.

Ensuring financial protection is quite essential in today's uncertain times. An endowment plan provides the death benefit to the assigned nominee/beneficiary in the event of the death of the insured. It helps the nominee or family to confront immediate financial loss, whereas an emotional loss will take the time to recuperate

Endowment policies help you to achieve the financial objectives or goals at different life stages.Proceeds received from the maturity benefits in the event you survive the policy term can be utilized in meeting such objectives.

By investing in an endowment plan, you are entitled to receive the lump sum amount at the maturity that you can utilize for meeting the financial goals of your life with ease.

By investing in an endowment plan, you can accumulate huge corpus at the maturity of the policy and can easily achieve your financial goals as well.

Everyone wants to lead a worry-free life. An endowment plan offers both the insurance and investment protection. Get the assured peace of mind. This plan offers life cover to the nominee in case of the demise of the insured, and the policyholder can get the maturity amount in case you survives till the end of the policy period.

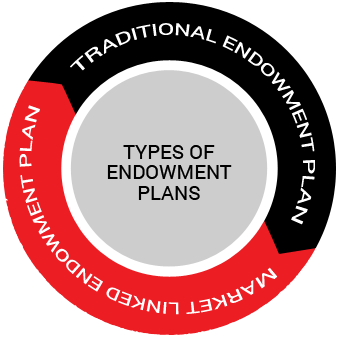

Typically, there are two types of endowment plans.

Traditional endowment plans are those plans that offer insurance plus investment under a single policy. Such plans are a long term life insurance contract where the policyholder has to pay premium throughout the tenure of the policy or may opt for single pay or limited payment option. The benefits under the policy are either paid out on the death of the life insured or at maturity, if the life insured survives the term of the policy. The death benefit paid under the plan is the sum assured plus the accrued bonus (if it is a with profit endowment policy) or only sum assured (if it is a non profit endowment policy) where as maturity benefits are sum assured plus accumulated bonus or guaranteed additions by the insurer.

Here the investment portion of the policy is taken care by the insurance company. The bifurcation of cost and benefits are not transparent in nature

Unit Linked Insurance plans (ULIPs) are also categorized as endowment plans as it offers the dual benefit of insurance and investment collectively under one policy. Such plans also offer death and maturity benefits (whichever occurs earlier). Part of the premium is taken away to provide insurance by deducting mortality charges, and part of it is kept aside for investment, which is decided by the policyholder as per his/her risk appetite and is based on market performance.

A fund is created which attracts returns as per the investment made in either equity or debt instrument which is paid as fund value to the policyholder at the time of maturity. If the policyholder dies during the tenure of the plan, Sum assured or higher of Sum Assured or Fund Value is paid to the nominees and the policy ceases after that.

ULIP's are transparent and flexible in nature, and the investment steering is in the hands of the policyholder and not the insurance company.

There are two types of bonus payouts available under an endowment plan.

A bonus payout which is declared on an annual basis by the insurer and it depends on the performance of the insurer. This payout is added to the funds and payable at the maturity or death of the life insured.

A type of loyalty bonus that reflects the performance of a ‘With Profit’ endowment policy and is paid at the maturity or the death of the life insured.

Following are the factors that help calculate the premium amount for an endowment policy.

Age plays a key role when it comes to calculating the premium amount. The age factor determines the premium amount charged towards the life cover in the endowment plan. If you buy the plan at an early age, you will be charged with the lower premium amount when compared to the one when buying the plan at a later age.

Consumption of alcohol, tobacco, and other nicotine products also affect the premium charged in the endowment plan. Intake of these products is injurious to health, and it increases the life risk of insured and thus, insurers charge higher premiums to cover the risk.

Your health status also determines the amount of premium to be paid by you. In case you possess severe illnesses such as diabetes, cancer, or high blood pressure, you will be charged with a higher amount of premium.

As per statistics, men have lower life expectancy than women and taking into consideration the life risk for men, insurers tend to charge them with the higher premiums for providing the life cover as compared to women.

If you are working in a risky industry such as working in Oil & gas, mining industry, fisheries, etc., and your nature of work involves risk to your life you will be charged with the higher premiums.

Following are the rider options to attach to your Endowment life insurance policy:

This rider ensures additional financial benefits to the nominee in case of death of the insured arising from an accident. The insurer pays the accidental death sum assured to the nominee, which is over & above the base sum assured of the policy.

This rider provides an additional death benefit to the nominee, which is additional to the base policy sum assured in the event of the death of the life insured.

This optional rider covers the medical costs incurred due to severe illnesses such as a Heart Attack, Cancer, and Major organ transplant, which may disable an individual that result in loss of earnings. Typically, the covered provided under this rider is the sum assured and paid additional to the sum assured in the base policy. The benefit under this rider is paid upon diagnosis of the illness.

This rider waives off all the future premiums in the event of death or disability of the life insured. The policy continues till its maturity. It enables the policyholder to enjoy benefits of the insurance policy, even when he/she cannot pay premiums.

By choosing this rider, the assigned nominee/family of the life insured is provided with the monthly income apart from the lump sum payout they get upon the death of the insured. The payout and other benefits are subject to the terms mentioned under the rider benefits.

This rider provides monthly income to the life insured in case of permanent or temporary total or partial disability arising due to an accident or illness. The payout differs and it depends on the kind of disability occurred.

Get QuotesYour endowment life insurance plan has the following exclusions.

It states that if the life insured commits suicide within the first year of the commencement of the policy, the insurance company is not bound to pay the policy proceeds.

This clause states that if the life insured dies while traveling in a private plane as a passenger, the insurance company is not liable to entertain the claim. The benefits of the policy are paid only when the life insured dies while traveling in a commercial plane crash.

It states that if the life insured dies due to the involvement in dangerous adventure activities such as river rafting, para-gliding, skiing, rock climbing, etc., the insurance company is not liable to pay the policy benefits.

This exclusion states that the insurer is not liable to pay if the life insured dies as a result of the war.