Get a call back!!

Get a call back!!

1800-12000-0055

Life is full of uncertainties. Apart from the risk of death, there is a risk of illness too. Certain diseases like cancer, stroke, and lung disease are life-threatening and may result in loss of income due to disability or severity of the disease. Treatment for such critical illnesses requires a lot of money, which can cause an imbalance in your savings and financial setup. Critical Illness Insurance plans provide lumpsum fixed benefits in the event the person is diagnosed with any of the critical illnesses listed in the critical illness insurance policy. It is a fixed benefit health plan which pays out a lumpsum amount.

There are various factors listed below that will illustrate the need to buy a Critical Illness Health Plan:

A Critical illness insurance plan can safeguard you from an enormous and cumbersome treatment expense. Extracting such huge amounts from your regular financial kitty may storm your financial stability. It pays a fixed amount opted under a plan that will help you get the treatment done without any worries.

A critical illness plan acts as a backup financial cover if adversities arise out of critical illness. The severity of critical illness is so much that it may result in loss of income due to poor health conditions and treatment costs which will make a massive hole in your pocket. With Critical Illness insurance, you may not have to pull money from your savings or other investments you have kept for other important purposes.

A Critical Illness Plan by your side will always keep you in solace. Suppose you are diagnosed with any of the listed critical illnesses under your plan. In that case, you know at the back of your mind that you will get fixed benefits from your policy without attaining any financial burden.

Some real-life stories depict that critical illness patients have such a deterrent impact that they almost lose all their savings, investment, and assets like cars, jewelry, house, etc., for getting the treatment done. Also, due to the severity of illness, there is a loss of income. Such scenarios disrupt the financial equilibrium and compel anyone to take loans or debts to maintain finances. Critical Illness Plan safeguards you from getting into loans or debts and provides you a fixed benefit for the treatment you may use as per your priorities.

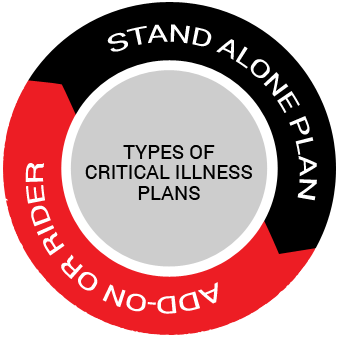

Critical Plans can be opted as

Critical Illness plan is available as a stand-alone individual policy offering critical illness benefits as a fixed payout depending upon the chosen Sum Assured in the diagnosis of a critical illness. Stand-alone plans cover a vast list of critical illnesses, varying from insurer to insurer. For a stand-alone critical illness plan, the sum assured can be taken as per your requirement and budget.

Protection against critical illness can also be taken as an add-on cover or as a rider along with the basic health insurance plan. Critical Illness rider will have restricted sum assured subject to the maximum base health insurance policy sum assured and cannot exceed the same. As an Add with the standard health plan, the number of critical illnesses covered is limited and not exhaustive.

Following are the key determinants for computing the premium amount for your Critical Illness Insurance Plan.

As the age progresses, the risk of getting an illness also increases. To accommodate the high risk based on age, the insurer charges a higher premium for higher ages to provide critical illness cover.

The higher amount of critical illness cover or sum assured demands a higher premium. For a critical illness cover of 15 lakh, the premiums will be more as compared to the critical illness cover of 5 lakh. The Higher the Sum assured, the higher will be your premium amount.

The past and present medical health conditions will also affect the premium under your policy.

Critical Illness policy has a minimum term of one year and can be renewed yearly to get continuous coverage. However, some plans come with 2 years or more as tenure and many insurers offer discounts on choosing the term for more than 1 year.

Following are the conditions/exclusions that are not included in your Critical Illness Health Plan.

• Any claim within the waiting period is not covered

• Any pre-existing diseases

• Treatment received outside India

• Medical treatment expenses for insured involved in any criminal act

• Medical Expenses related to self-inflicted injury like attempted suicide

• Medical Expenses occurring medical treatments due to alcohol or drug use

• Medical expenses for the treatment of AIDS

• Expenses related to pregnancy and childbirth

• Congenital disease

(Exclusions may differ from one insurer to another and plan to plan.)