Get a call back!!

Get a call back!!

1800-12000-0055

Reliance Nippon Life Premier Wealth Insurance Plan is a non-participating unit linked insurance plan that helps cater your protection and investment needs. This plan helps create wealth through wealth boosters and thereby, you can easily meet your long-term financial goals.

Get QuotesThis policy offers following 6 investment funds and you have the option to invest in any one or combination of fund options.

You have the option to choose from following two investment strategies that help manage your funds.

Self-Managed Option: This investment strategy provides you the flexibility to invest amongst 6 available investment funds. With this investment strategy, you can avail switching and premium re-direction facility.

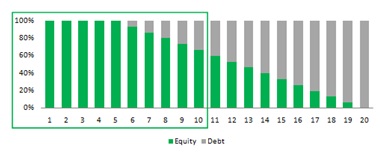

Auto-Managed Option: This option suits best to you, in case you want automated options to manage your investments. Under this investment strategy, you can opt for Target Maturity Option (a tailor-made solution through automatic asset allocation between equity and debt) or Life Stage Option (maintain a balance between equity and debt basis on your life-stage).

In case of unfortunate death of the life assured while the policy is in-force, the Death Benefit payable is higher of Base Sum Assured less partial withdrawals#, 105% of the total premiums paid, or Base Fund Value.

In case of top-up premium, it is higher of all top-up sum assured, 105% of all the top-up premiums paid, or top-up fund value.

#Before age 60 years of the life insured, Base Sum Assured is reduced to the extent of Partial Withdrawals made during the last two years prior the date of death. After attaining 60 years of age, Base Sum Assured is reduced to the extent of all Partial Withdrawals made after attaining 58 years.

On survival of the life insured till the end of the policy term, the Total Fund Value including top-up fund value is payable at maturity. You can receive this benefit as a lump sum or through a structured payout by using ‘Settlement Option’.

On maturity, you can opt to receive your money in annually, semi annually, quarterly or monthly installments for a maximum period of 5 years, after the date of maturity. You also have the option to completely withdraw the fund value at any time during the settlement period. No life cover is applicable during this settlement period. Partial withdrawals and switches are not allowed during the settlement period.

It is available in the form of additional units are added under the policy, starting from the end of 8th policy year. Each Wealth Booster is expressed as a percentage of the average of daily Fund Value in preceding 12 months of the Base Plan in the same Policy Year and it is 0.30%/0.50% per annum for regular & limited pay/single pay, respectively. Once credited, Wealth Boosters cannot be taken back by the company.

Facility for Top-up Premium is available through the entire policy term, except during the last five years of the policy. The minimum top-up premium allowed is Rs 10,000. The total top-up premium should not exceed the total of base premiums paid at that point of time.

Top-up Sum Assured = Top-up Multiple * Top-up Premium

Top-up multiple is 1.25/1.10 times for age less than 45 years/age equal to 45 years & above, respectively.

You can switch among 6 available fund options to suit your changing investment needs. This option is available, when opted for self-managed option.

Premium Re-direction facility is available to alter future premium allocation and it will apply to your subsequent premiums. This option is not applicable for single premium option.

Partial Withdrawal is allowed from 6th policy year onwards (in case of minor lives, life assured attains 18 years). The minimum partial withdrawal amount allowed is Rs 10,000.

The maximum partial withdrawal amount allowed shall not exceed 25% of the total fund value (including top-up fund value), provided the fund balance post such withdrawal should be at least equal to 125% of annualized premium or 25% of single premium (single pay).

You have the option to increase or decrease the sum assured any time during the policy term, by giving prior notice to the company 30 days prior the policy anniversary. Any increase in sum assured is allowed before the policy anniversary on which the life assured attains 60 years of age.

The Non-Negative Claw Back Additions are available at various intervals of time, after the first 5 years under the policy.

The plan is not eligible for the bonuses, as it is a non-participating insurance plan.

No loan benefit can be availed under this plan.

Upon surrendering the policy with-in the lock-in period of 5 years, the Fund Value (including top-up fund value) less applicable discontinuance charges is credited to the ‘Discontinued Policy Fund’ and it is refunded upon completion of the lock-in period. A fund management charge of 0.50% per annum of the Discontinued Policy Fund is applicable. The proceeds after addition of interest subject to a minimum guaranteed interest rate of 4% per annum or as stipulated by IRDAI is payable after the end of the lock-in period.

Upon surrendering the policy after completion of the lock-in period, the Fund Value (including top-up fund value) as on the date of surrender is payable immediately.

| Factor | Minimum | Maximum |

| Age (as on last birthday) | 30 Days | 60 Years |

| Age at Maturity | 18 Years | 70 Years |

| Policy Tenure | 10 Years (Regular/Single Pay), 10 Years (Limited Pay- 5/7 Years), 15 Years (Limited Pay- 10 Years) | 30 Years |

| Premium Paying Term (PPT) | Regular/Single/Limited Pay Term (5/7/10 Years) | - |

| Premium Paying Mode | Single, Annually, Semi Annually, Quarterly & Monthly | - |

| Annual Premium Amount | Rs 2,00,000 (Regular/Limited Pay), Rs 5,00,000 (Single Pay) | No Limit |

| Sum Assured | Regular/Limited Pay: >&=44 Years- Higher Of 10 Times The Annualized Premium Or 0.5 * Policy Term * Annualized Premium For 45 To 60 Years - Higher Of 7 Times The Annualized Premium Or 0.25 * Policy Term * Annualized Premium Single Pay: >&=44 Years- 1.25 Times The Single Premium For 45 To 60 Years – 1.10 Times The Single Premium | Regular/Limited Pay: >&=30 Years- 30 Times The Annualized Premium For 31 To 40 Years- 20 Times The Annualized Premium For 41 To 44 Years – 15 Times The Annualized Premium For 45 To 50 Years –15 Times The Annualized Premium For 51 To 55 Years –12 Times The Annualized Premium For 56 To 60 Years –10 Times The Annualized Premium Single Pay: 1.25 Times The Single Premium (For Ages Up To 44 Years & 45 To 60 Years) |

| Freelook Period | 15 Days/30 Days (for Distance Marketing Channel) From The Receipt Of The Policy | - |

| Grace Period | 30 Days (15 Days For Monthly Mode) | - |

| Plan Type | Offline | - |

No rider is available under this plan.

Premium Allocation Charges: This charge is deducted from the premiums paid and the balance amount is then allocated to funds chosen. For regular/limited pay, the Premium Allocation Charge is 4%/3%/2.75%/1.50% or 1st policy year/2nd to 4th policy year/5th policy year/6th policy year & onwards, respectively. For single pay, the Premium Allocation Charge is 1.5%/1% for single premium amount of less than Rs 10,00,000/Rs 10,00,000 & above, respectively. For top-up, the Premium Allocation Charge is 1% of top-up amount.

Policy Administration Charge: Policy administration charge is Rs 300/Rs 200 for regular & limited pay/single pay, respectively subject to a maximum of Rs 500 per month.

Mortality Charges: Mortality charge is based on the age of the life insured, life insurance cover, occupation of life insured, health of life insured, and the fund value. This charge is deducted every month by cancellation of units.

Fund Management Charges: Fund management charge levied is a percentage of the Fund Value. It is 1.35% p.a for Life Equity Fund 3, Life Pure Equity Fund 2, & Make in India Fund, 1.25% p.a for Life Balanced Fund 1, Life Corporate Bond Fund 1, & Life Money Market Fund 1, 0.50% p.a for Discontinued Policy Fund.

Discontinuance Charge: This charge is levied, in case the policy is discontinued during the first 4 policy years. This charge is levied as applicable under the policy terms & conditions. For more details, please refer the policy brochure.

Switching Charge: 52 free switches are available free of cost during a policy year. A charge of Rs 100 is levied when opted for subsequent switching in the same policy year, subject to a maximum of Rs 500 upon prior approval from IRDAI. No option is there to carry forward the unused switches.

Partial Withdrawal: 2 free partial withdrawals are allowed during a policy year. A charge of Rs 100 is levied when opted for subsequent withdrawal in the same policy year, subject to a maximum of Rs 500 upon prior approval from IRDAI. No option is there to carry forward the unused partial withdrawals.

Medical Examination Expenses: These expenses in case of revival of the policy will be borne by the policyholder.

Taxes: The charges mentioned under this plan are subject to applicable tax and cess, as applicable.

Tax benefits can be availed under section 80C & 10(10D) under the Income Tax Act, subject to change in tax laws.

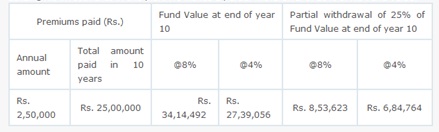

Mr. Praveen is looking to invest with a plan that can help accumulate the wealth. He chooses to buy Reliance Nippon Life Premier Wealth Insurance Plan having policy term of 20 years (regular pay), annual premium of Rs 2,50,000 and sum assured of Rs 25 Lacs.

Scenario 1: Praveen opts for Target Maturity Option under Auto-Managed options. This strategy automatically manages his investments by changing the allocation between the debt and equity funds.

Scenario 2: Praveen opts for the Self-Managed option. He decides to invest in Life Equity Fund 3 and stays invested till maturity of the policy. Following is the expected benefit as received by him:

Scenario 3: After investing in the Life Equity Fund 3 for 3 years, he switches his investment to Life Corporate Bond Fund 1. He thus locked in the returns from the rise in the equity markets and is now enjoying stable returns from the bond market.

Scenario 4: At the end of the tenth policy year, Praveen decides to purchase a new car by utilizing his investments in this plan. He makes a partial withdrawal of 25% of his Fund Value at the end of 10th year.

Scenario 5: In the third policy year, Praveen dies in an unfortunate accident. His wife, who is his nominee, gets the Death Benefit.