Unit Linked Insurance Plan – An Ideal Investment cum Insurance Plan

Life insurance plans are of different types suiting different needs and goals of the individuals. One such category of a life insurance plan is Unit Linked Insurance Plan (ULIP) suited best for wealth creation to meet different financial goals in one’s life.

Table Content

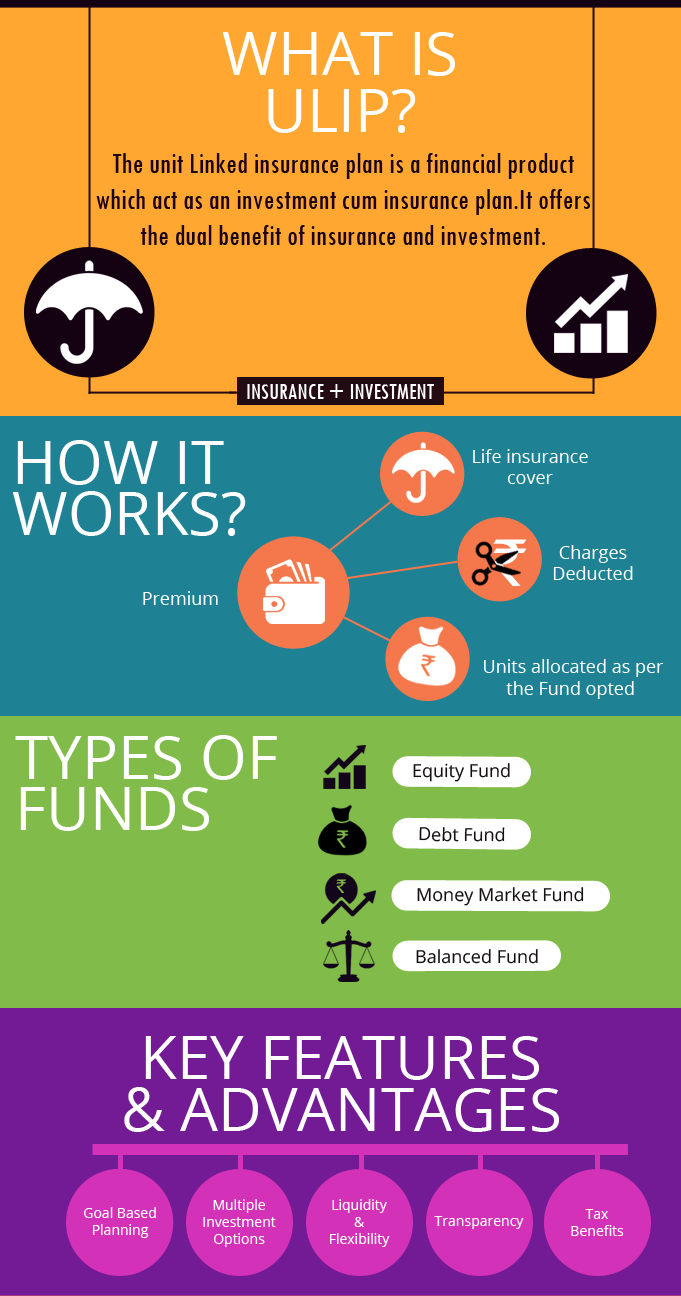

What is Ulip and How it works?

The Unit Linked Insurance Plan (ULIP) is a financial product which acts as an investment cum insurance plan.Ulip offers the opportunity of wealth creation along with a life cover to protect your loved ones financially. It offers the dual benefit of insurance and investment. The minimum life cover under Ulip which a policyholder gets is 10 times of the annual premium.

The premium amount you pay is partly diverted towards buying a life insurance cover and remainder amount is assigned to a common pool of money called fund, after deducting various charges associated with ulip. Investment is done as per the asset class chosen by the policyholder based on his risk apetite. The fund options for investment are equity based fund, debt based fund and/or the balanced/hybrid fund (which is a combination of debt and equity). Post investment in the chosen fund or funds, units are allocated based on the applicable Net Asset value( NAV) of the respective fund as per the date of investment.

| NAV is calculated as (Market value of investments held by the fund + Value of current assets – value of current liabilities)/ number of units existing on valuation date. Net asset value is declared every day based on the performance of the fund.NAV is different for different funds available under a ulip for investment. Fund Value is the total value of a particular fund, which is calculated by multiplying number of units in the fund with the net asset value (NAV) of the fund on that particular day. |

Let us understand it with an example:

Suppose a policyholder’s annual premium is Rs 100,000 for 20 years, with a sum assured of Rs 10 Lakhs. After deduction of applicable charges of Rs 3,000 the amount of Rs 97,000 is invested in the fund chosen by the policyholder. Assuming the fund’s NAV is Rs 10 on the day he invested, so he is eligible to get 9700 units(Rs 97,000/NAV of Rs 10).

Key Features and Adantages of ULIP

Goal Based Planning: Ulips are best suited to meet your future financial goals such as wealth creation,for child’s higher education, retirement planning,etc. There are ulips which are custom made to suit your specific financial goal apart from offering you a life insurance cover. There are Child ulips, retirement ulips,wealth creation ulips which work on the basic model but have salient features to accelerate your goal based planning by creating an adequate corpus on maturity.

Multiple Options for investment: To suit various policyholders with a different risk apetite, unit linked insurance plan offers multiple fund options varying from debt,equity, balanced fund. Based on the risk bearing capabilities, financial goals and the term of the policy, the policyholder can invest in one or more funds as per his suitability. So, if you want to raise your wealth and won’t hesitate taking risk on your investment, you can invest in equity funds. Similarly, if you want to gain steady returns on your investment, you can invest in debt funds.

Liquidity: The unit linked insurance plan offers liquidity in the form of “Partial Withdrawals”. Partial withdrawal allows you to withdraw some portion out of your fund value created after a specified time period. There is a minimum and maximum limits defined for such withdrawals which may vary from one plan to another.

Flexibility: The unit linked insurance plan offers flexibility by offering the benefit of switching and redirection. Switching allows you to change your existing proportion of investment from one fund to another due to the market fluctuations , your changed risk apetite ,etc. Redirection on the other hand, allows you to define the investment proportion into different funds for your future investments, keeping your existing investment set up intact. This feature makes ulip different from other investment instruments as this feature is not available in mutual funds or any other kind of financial instruments. This facility is usually free of charge for most of the unit linked plans or attract nominal charges, if applicable.

Transparency: The unit linked insurance plan is a transparent financial product as the policyholder can easily see how much money is deducted for various charges, how much money is invested, what is the return on investment, what is the fund value at any point of time, etc. There is nothing hidden under the structure or functioning of ulips which makes it more viable and informed product for the policyholder.

Tax Benefit: The premium paid for a unit linked insurance plan qualifies for a tax deduction upto Rs 1.5 Lakhs under Section 80 C of the Income Tax Act, 1961. The maturity proceeds are also tax-free under Section 10(10D) of the Income Tax Act.

Types of Funds Available under ULIP

Most of the life insurance companies offer multiple options of funds to suit the investment needs, risk apetite and time horizons for the policyholder. Different funds offer different risk profiles for the policyholder. The return potential varies from one fund to another. Ulip funds are categorized by risk characteristic and investment objective. The returns in ulips are not guaranteed and is market linked. The risk and reward of the investment are borne by the policyholder. There are fund managers who decide and monitor about the actual investments done for the collective pool of money for a particular class of fund. One can invest proportionately in more than one fund as well under ulip. The nomenclature of the funds might vary from insurer to insurer, but the basic categorization of the funds available are as follows.

Equity Funds: The investment made in these kind of funds is further invested in high risk equities, shares and stocks of the companies traded in the stock market. These funds are also known as the growth funds. The return on investments is maximum here if the stock markets perform well. This kind of fund is suitable for the people with high to medium risk apetite.

Debt Funds: The investment made under these kind of funds is done in bonds, government securities (like gilts or corporate bonds), fixed income securities,etc. The risk involved is low to medium and the return on investment is also moderate. The risk is extremely low due to the fact that the Govt. securities or corporate bonds are always issued as fixed-income bearing instruments. This kind of fund is suitable for the people with low to medium risk apetite.

Money Market Funds: The investment made in such a fund is primarily done in bank deposits and money market instruments. These kind of funds are also known as cash funds. This fund is the lowest risk bearing fund equivalent to zero risk which offers lower returns as compared to the above mentioned two funds.

Balanced Funds: As the name suggests the investment made in such funds are balanced, which means the money is invested both in equities and debts. Such funds also give a balanced return to the policyholder as the risk is also balanced out with the amalgamation of high risk equity investment and low risk debt investment. The returns are high to moderate with medium risk involved under balanced funds.

| Types of Fund | Risk Involved | Return on Investment |

|---|---|---|

| Equity Funds | High | High |

| Debt Funds | Medium to low | Moderate |

| Money Market Funds | Low | Low |

| Balanced/Hybrid Funds | Medium | High to Moderate |

Types of Charges associated with ULIP

There are various charges attached to a unit linked insurance plan.

Premium Allocation Charges: These charges are upfront charges which are deducted from the premium amount paid by the customer. These charges are deducted on account of the initial expenses (such as cost of underwriting, medicals & expenses related to the intermediary’s commission,etc.) incurred by the insurance company in issuing the policy. Such charges are high in the first few years and later reduce or diminish for many plans.

Mortality charges: These charges are deducted to offer you the death cover under a ulip. Mortality charges are deducted on a monthly basis and are based on various factors such as age of the policyholder, their health status, Life coverage amount, etc. Mortality charges are lower for lower age groups and higher for the higher age bands.

Policy Administration Charges: These charges are deducted on a monthly basis by cancelling units to recover the expenses incurred by the insurance company in servicing and maintaining the policy like paperwork,cost of sending reminder notices,issuing ulip statements on a regular basis, etc. They could be same throughout the policy term or may vary at a pre-determined rate as mentioned in the policy

Fund Management Charges: These charges are extracted for managing your investments under various funds, and are charged as a percentage of the assets’ value. Fund management charges are higher for equity based funds in comparison to debt-oriented funds. Insurance regulator IRDAI has set a cap of 1.35% per annum on fund management charges and it could not go beyond this limit for managing a fund under ulip. However, as the value of the investment grows over time, fund management charges may increase.

Surrender Charges: There is a lock in period of 5 years under ulip to surrender a policy. If the discontinuation of the policy is within first five years of inception, applicable surrender charges are levied for early surrender. The surrender charges could not go beyond Rs 6,000 as set by the regulator. However, post completion of the lock in period, there are no surrender charges applicable.

Switching/Redirection Charges: Usually, a limited number of fund switches are allowed each year without charge, but with subsequent switches, applicable nominal charge may be levied.

ULIP Reforms by IRDAI for Making it Customer Friendly Financial Product

Reforms introduced were to keep an eye on the unrestricted charges and commissions which extracts the maximum amount of premium and allowing the lesser amount for investments for the policyholder.

- The lock in period of the Ulip has been increased from 3 years to 5 years.The intention is to keep the policyholder invested for a longer tenure for better returns as ulip will fetch rewarding returns if invested for a longer time period.

- Reduction in premium allocation fees as prior to September 2010 commissions were 30-35% of the premiums you paid in the initial years of the policy. Now, only 8-10% goes to the life insurance agent as a commission through premium allocation charges.

- For the policyholder aged less than 45 years of age, the death benefit or sum assured offered is minimum 10 times the annual premium paid. For more than 45 years of age the death benefit is 7 times the premium paid each year. The death benefit at any time cannot be less than 105% of the total premiums paid by the policyholder .

- Ulips with policy term more than 10 years, the maximum charges collectively cannot be more than 2.25% of the annual premium.

- The maximum surrender charges cannot be more than Rs 6000 if the policyholder surrenders in the lock in period.

Final Words

To look for growth in your invested hard earned money is a genuine aspiration for an individual. For wealth creation and getting a life cover, you can rely on ULIPs to grow your money sustainably. ULIP fulfills growing need of investors looking for asset allocation with an intent of augmentation and gaining the benefits of money markets. Ulips help investors to participate in the boom of the capital market, thereby growing their investments if invested for a longer tenure. It is important to buy a unit linked plan based on your goal setting, risk apetite and for a longer tenure to reap the optimum benefits under this investment cum insurance plan.