Tax Deductions on Home Loan

Buying a house is one of the key decisions in life. However, it becomes quite challenging when it comes to arranging the finances to buy a house. The property prices continue to grow steadily.

| The Housing Price Index (HPI) as released by RBI recorded a growth of 8.7% during the 1st quarter (April to June) of 2017 over the 1st quarter of the previous year. All-India HPI also witnessed an increase of 0.4% during 2nd quarter over 1st quarter in the year 2017-18. |

Considering the statistics of property prices in India, it’s advisable to invest in the real estate as early as possible that would help you own an immovable property for you & your family. When you are seeking to buy a home, taking a HOME LOAN can make your dream come true. A home loan provides the mortgage that will help you to purchase/construct a new house and renovation/re-construct an existing house. Banks and housing finance companies offer home loan at an attractive and low interest rates.

Table Content

Why you should take a home loan?

Taking a home loan offers you several key benefits.

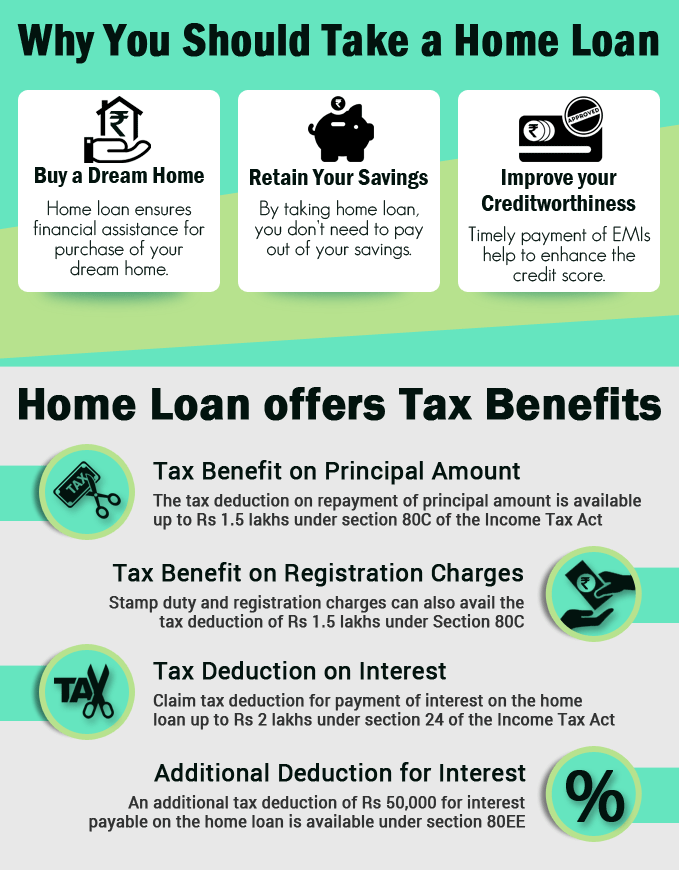

- Buy a Dream Home: In case, you decide to pay the money upfront, you will have a restricted budget and will not be able to buy the desired home. A home loan provides you the flexibility to go beyond your set budget and look for better property options in your desired location.

- Tax Benefits: You can claim a tax deduction of Rs 2 lakhs on the interest payable on the home loan during a financial year, under section 24 of the Income Tax Act. You can also avail a tax deduction of Rs 1.5 lakhs on principal repayment, under section 80C of the Income Tax Act.

- Save for Contingencies: Don’t put all your eggs in one basket. In financial perspective, it infers that you should not put your entire savings into a single investment.In case, you don’t take the loan and buy a home from your savings; a considerable sum gets locked in. By taking a home loan, you can retain your savings that will come to rescue during times of emergencies. Moreover, you can diversify your investment portfolio and enhance your returns, rather than locking in your money in real estate investment.

- Improve your Credit History: A home loan helps you build the credit worthiness. The timely payment of home loan EMIs will have a positive effect on your credit score. With a high credit score, you can quickly get approvals on loan and credit card applications.

You can avail tax benefits for 2 different components, including, repayment of the Principal Amount and payment of Interest.

Tax Benefit on Principal Amount

The tax deduction on repayment of the principal amount is available up to Rs 1.5 lakhs within the overall limit of section 80C of the Income Tax Act, 1961.

Conditions to Avail the Tax Deduction:

- The tax benefit on repayment of the home loan is allowed only after the construction is complete and you have received the certificate for the same.

- The house property must not be transferred before 5 years from the end of the financial year in which you have obtained its possession. Upon transferring the property before 5 years, no tax deduction on the home loan shall be allowed under Section 80C. The tax deduction already claimed shall be considered as the income in the year during which the property has been sold, and you (assessee) will be liable to pay tax on such income.

Tax Benefit on Registration Charges

Stamp Duty, Registration Fee and other related expenses are also eligible to avail the tax deduction up to Rs 1.5 lakhs under Section 80C of the Income Tax Act. You can claim the tax deduction in the same year you make the payment towards such expenses.

Tax Deduction on Interest Payable

You can claim tax deduction towards payment of interest on the home loan up to Rs 2 lakhs w.e.f FY 2014-15 (1.5 lakhs when filing returns for FY 2013-14 or before) under section 24 of the Income Tax Act. This tax deduction can be availed when the property is self-occupied or when it is left vacant.

In case you have rented out the property, the entire interest amount payable on the home loan is allowed as a tax deduction under section 24 of the Income Tax Act. Your tax deduction on interest will be reduced to Rs 30,000, if the purchase or construction of the property is not completed within 5 years (3 years for FY 2015-16 or before) from the end of the financial year during which the loan was taken.

Deduction on home loan interest can be claimed only after the construction is finished.

Additional Deduction for Interest on Home Loan

Section 80EE allows an additional tax deduction of Rs 50,000 for interest payable on the home loan. This tax benefit would be available over and above the tax deduction of Rs 1.5 lakhs under Section 80C and Rs 2 lakhs under Section 24. This benefit is applicable exclusively for first time home owners.

Conditions to Avail the Tax Deduction:

- The value of the house is up to Rs 50 lakhs.

- Loan taken is Rs 35 lakhs or less and has been sanctioned by a financial institution or a housing finance company.

- Loan has been sanctioned between April 1st 2016 to March 31st 2017.

You can claim tax benefits by furnishing the interest certificate from the bank and a loan account statement that specifies the amount paid towards principal, interest and prepayment of principal (if any).

Know Your Eligibility

People who have a regular source of income, i.e., salaried professionals and those who own the business (self-employed individuals) are eligible to take the home loan.Before you apply for a home loan, you can determine the loan amount you are eligible for, which depends on your repayment capacity. Your repayment capacity is determined on the basis of your monthly disposable income, which can be computed by total monthly income less monthly expenses. Your loan repayment capacity also depends on other factors such as spouse’s income, assets, liabilities, etc.

The bank asks for your income proof to assess whether you are able to repay the loan. Banks usually consider that your monthly disposable income is available for loan repayment. If you are running with existing liabilities, the eligibility goes down further. Banks usually cap the loan amount at 80-90% of the total property value, that varies from one bank to another.The loan tenure usually don’t go beyond the retirement age, so the banks and other financial institutions sanction loan for your earning years only.

Interest Rates

Home loan interest rates are of two types, fixed and floating.In case of fixed rate, the interest rate remains fixed through the entire loan tenure and it does not change with market fluctuations. With a fixed interest rate, you can have a clear idea of your EMI obligations. It is usually capped at 1% to 2.5% higher than floating rate.The floating interest rate varies as per the market conditions. This interest rate is linked to bank’s Marginal Cost of Lending Rate (MCLR) or the NBFC’s base rate. The floating interest rate is usually lower than fixed interest rate.

Most of the home loan applicants opt for floating interest rate. Various banks and other home loan lenders have come up with floating interest rates as low as 8.35%.

| Bank Name | Floating Interest Rate |

|---|---|

| SBI | 8.30-8.60% |

| HDFC Bank | 8.35- 8.55% |

| ICICI Bank | 8.35- 8.80% |

| LIC Housing | 8.35- 8.80% |

| PNB Housing Finance | 8.35- 9.25% |

Final Words

With the ever rising property prices, buying a home has become a tricky task. Home loans, however, help you to make your dream of buying a home come true. By taking a home loan, you don’t need to put all your savings in buying the property, rather you can put it into investment instruments that will facilitate you to generate returns as well. Home Loans also help you to avail various tax benefits under section 80C and section 24 of the Income Tax Act.