Post-retirement, a regular monthly income ceases and in order to continue the current lifestyle, one needs to make proper financial arrangements to stay financially independent after retirement. Enrollment in Pension/Retirement schemes can ensure a financially independent life to lead. A regular pension serves as a means of financial stability and security, during the post-retirement life. A pension scheme helps you to accumulate savings and get a regular income after retirement.

Table Content

- Increasing Life Expectancy

- Brief about National Pension System (NPS)

- Benefits of Investing in the National Pension System (NPS)

- Tax Benefits under National Pension System (NPS)

- 1. NPS Tax Deduction under Section 80CCD (1)

- 2. NPS Tax Deduction under Section 80CCD (2)

- 3. NPA Tax Deduction under Section 80 CCD(1b)

- Snapshot of Tax Benefits Under NPS

- Tax Exemption on Various Types of Withdrawals

- 1. Withdrawals at Retirement/at 60 years

- 2. Withdrawal before Retirement

- 3. Withdrawal Upon the death

- 4. Partial Withdrawals

- Bottom Line

- Related posts:

Increasing Life Expectancy

The life expectancy is increasing in India and you may need to accumulate more wealth to fulfill your post-retirement needs.

| As per United Nations Population Division, the world’s life expectancy is estimated to reach 75 years by the year 2050 from the present level of 65 years. According to statistics released by the World Bank, life expectancy in India in 2015 is 68 years compared to 41 years in 1960. In 2011, life expectancy in India was 62.3 years for males and 63.9 years for females and in 2015, it is 67.3 years for males and 69.6 years for females. Life expectancy in India is increasing at a fast pace. |

It is thus evident that people tend to live longer. The rising life expectancy, increasing cost of living, and inflation make retirement planning an essential part of your financial plan when it comes to ensuring financial security during post-retirement life.

Brief about National Pension System (NPS)

In order to provide retirement income to all the citizens, the Government of India launched the National Pension System (NPS) on January 1, 2004. NPS is an attractive long-term savings avenue, which offers safe and reasonable market-linked returns and thereby, helps you to effectively plan for retirement. NPS is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) and it aims to develop and regulate the pension sector in the country.

On 1st May 2009, PFRDA provided this pension system to all citizens of India, including the unorganized sector workers. With effect from December 2011, NPS has also been launched to the employees of the corporate sector. One needs to contribute regularly during his/her working life and on retirement, you can withdraw up to 60% of corpus as a lump sum and utilize the remaining 40% of corpus to purchase an annuity that will provide you a regular income (pension) after retirement. In addition to providing financial security for your post-retirement life, NPS also offers significant tax benefits.

A resident or non-resident Indian can join NPS between 18 to 65 years and can continue up to the age of 70 years in NPS.

Benefits of Investing in the National Pension System (NPS)

| Design Your Own Portfolio: A subscriber enjoys the flexibility to choose between auto choice and active choice that facilitates him/her to choose their own portfolio for investment under the NPS. Wide Array of Investment Options: NPS offers a wide range of investment options such as equity funds, corporate bond funds, government bond funds, and alternate investment funds, along with the flexibility to choose Pension Fund Manager which facilitates you to manage and grow your investments. Simple & Easy Process: The procedure for opening a pension account with NPS is quite simple. It can be done online or offline easily. Portable & Regulated: Pension Fund Regulatory and Development Authority (PFRDA) is the regulatory agency for NPS, and aimed to ensure transparent investment norms and regular monitoring of fund managers. |

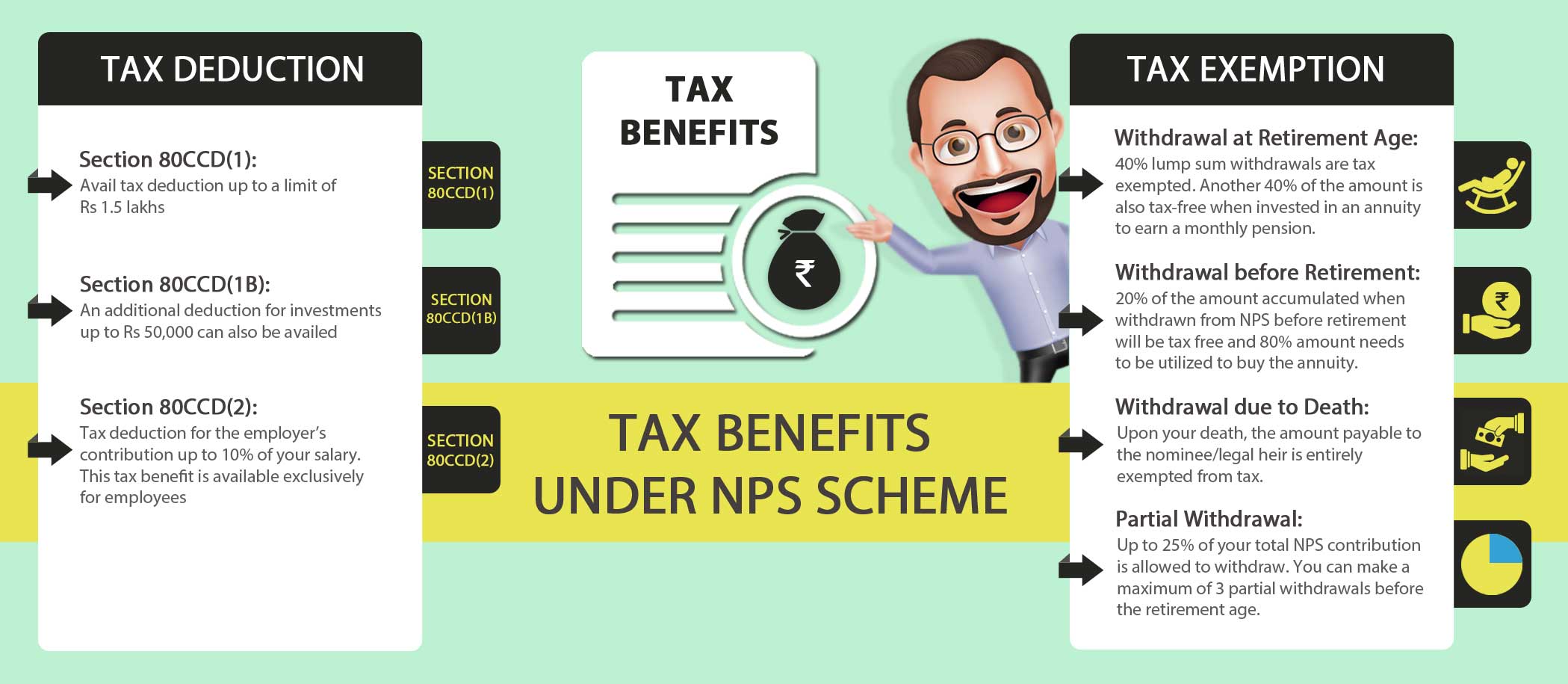

Tax Benefits under National Pension System (NPS)

1. NPS Tax Deduction under Section 80CCD (1)

The maximum tax deduction available under this section is up to a limit of Rs 1.5 Lakhs. This is part of the overall deductions under Section 80 C of the Income Tax Act,1961.

For Salaried Individuals: Employee’s mandatory contribution to NPS for retirement savings up to 10% of the basic salary and dearness allowance (DA) is eligible for up to 1.5 Lakhs is eligible for a tax deduction.

For Self Employed Individuals: Such cadre of taxpayers can contribute up to the limit is 10% of their annual income up to a maximum of Rs 1.5 Lakhs.

2. NPS Tax Deduction under Section 80CCD (2)

The employers’ contribution of up to 10% of the basic salary plus DA of the employee is eligible for deduction under this section. The employer’s contribution to NPS gains tax deduction under this section which is over and above the maximum limit of 1.5 Lakhs under Section 80 C.

For Salaried Individuals: The tax deduction under this section is available for salaried individuals only. The employer’s contribution up to 10% of basic plus DA is eligible for deduction under this section. Additional deduction by the employer towards NPS also offers benefits to the employer as it can claim tax benefit for its contribution by showing it as a business expense in the profit and loss account.

The upper limit under this section is lower of the three values

- The actual amount contributed by an employer,

- 10% of the Basic salary+DA of the employee

- Gross Total Income of the employee

For Self Employed Individuals: The tax deduction under this section is not available for the self-employed taxpayers as the deductions can be availed only if the employer contributes additional amounts towards NPS for the employer.

3. NPA Tax Deduction under Section 80 CCD(1b)

Under this section, an additional tax benefit of Rs 50,000 is available for voluntary investment under National Pension System. The tax deduction under this section is over and above the tax deduction limit of Rs 1.5 Lakhs. This section was introduced in the Budget 2015-16 and prior to this, it was not available.

For Salaried Individuals: Additional deduction of Rs 50,000 under this section is available to the salaried taxpayers over and above the limit of Rs 1.5 Lakhs.

For Self Employed Individuals: This additional deduction of Rs 50,000 under the Section CCD (1B) is available to salary as well as self-employed taxpayers both.

Snapshot of Tax Benefits Under NPS

| Sections | Deductible under NPS | Maximum Deduction under NPS |

|---|---|---|

| Section 80 CCD (1) | Mandatory Deduction from Salary towards NPS | Rs 1.5 Lakhs |

| Section 80 CCS (2) | Voluntary Deduction from Salary towards NPS | 10% of basic salary + DA |

| Section 80 CCD (1b) | Voluntary contribution by individuals toward NPS | Rs 50,000 |

| Total Deduction under NPS | The total maximum benefit an individual can avail of is Rs.2 Lakhs (where Rs.1.5 Lakhs will be part of Sec.80C limit) |

Tax Exemption on Various Types of Withdrawals

Following are the withdrawal/exit options available in NPS, which enjoys tax exemption as well.

1. Withdrawals at Retirement/at 60 years

You are allowed to withdraw up to a maximum of 60% of the accumulated corpus at the retirement age. 40% of the total accumulated NPS amount is tax exempted as it has to be compulsorily used to purchase an annuity. It means, that if you withdraw 60% of the NPS corpus, your 40% amount will be tax-free and you need to pay tax only on 20% of the accumulated money. The income from an annuity will be taxed year on year as per your tax slab. The pension amount received is considered as income and thus taxable in the year of receipt, as per prevailing income tax laws.

2. Withdrawal before Retirement

If you want to completely withdraw from NPS before retirement or the age of 60, the amount withdrawn will be tax-free, but you are restricted to withdraw up to 20% of the accumulated corpus and 80% of your wealth needs to be utilized to buy the annuity.

3. Withdrawal Upon the death

In the unfortunate event of your death, the amount withdrawn will be exempted from tax. The accumulated corpus in NPS would be payable to your nominee/legal heir. Upon the demise of government employees, the nominee needs to purchase the annuity and the entire amount as a lump sum cannot be withdrawn.

4. Partial Withdrawals

Partial withdrawals from NPS are tax-free, with effect from the financial year 2017-18. NPS comes with the option to make up to a maximum of 3 partial withdrawals before the age of retirement or 60 years of age. The partial withdrawal shall be allowed for the higher education of children,/marriage, treatment of specified diseases, or purchase/construction of the residential house.

You are allowed to withdraw up to 25% of your total NPS contribution. In order to get partial withdrawals, you need to invest in NPS for at least 10 years. Moreover, after the 1st withdrawal, you have to wait for at least 5 years to make a further withdrawal, except for treatment of the specified illness/s.

Bottom Line

NPS investment is largely focused on your retirement. You need to start investing from a young age say at 25-30 years, so you can easily accumulate a big corpus to fulfill your post-retirement needs. It is imperative to understand the tax deductions under various sections above to get the maximum tax deductions. Planning for post-retirement is always important and should be planned in a thought-through way.