Important Income Tax Deductions for FY 2019-20

Tax Planning is an important task for a tax payer to avail various tax exemptions, deductions and benefits to minimize the tax liability. Tax planning in imperative for everyone,whether you are salaried, self employed, or a professional. Tax deductions are allowed under Income Tax Act,1961 which enables you to save tax and reduce the tax burden. By subtracting tax deductions from your gross annual income, you will have a lesser income coming under the tax frame.

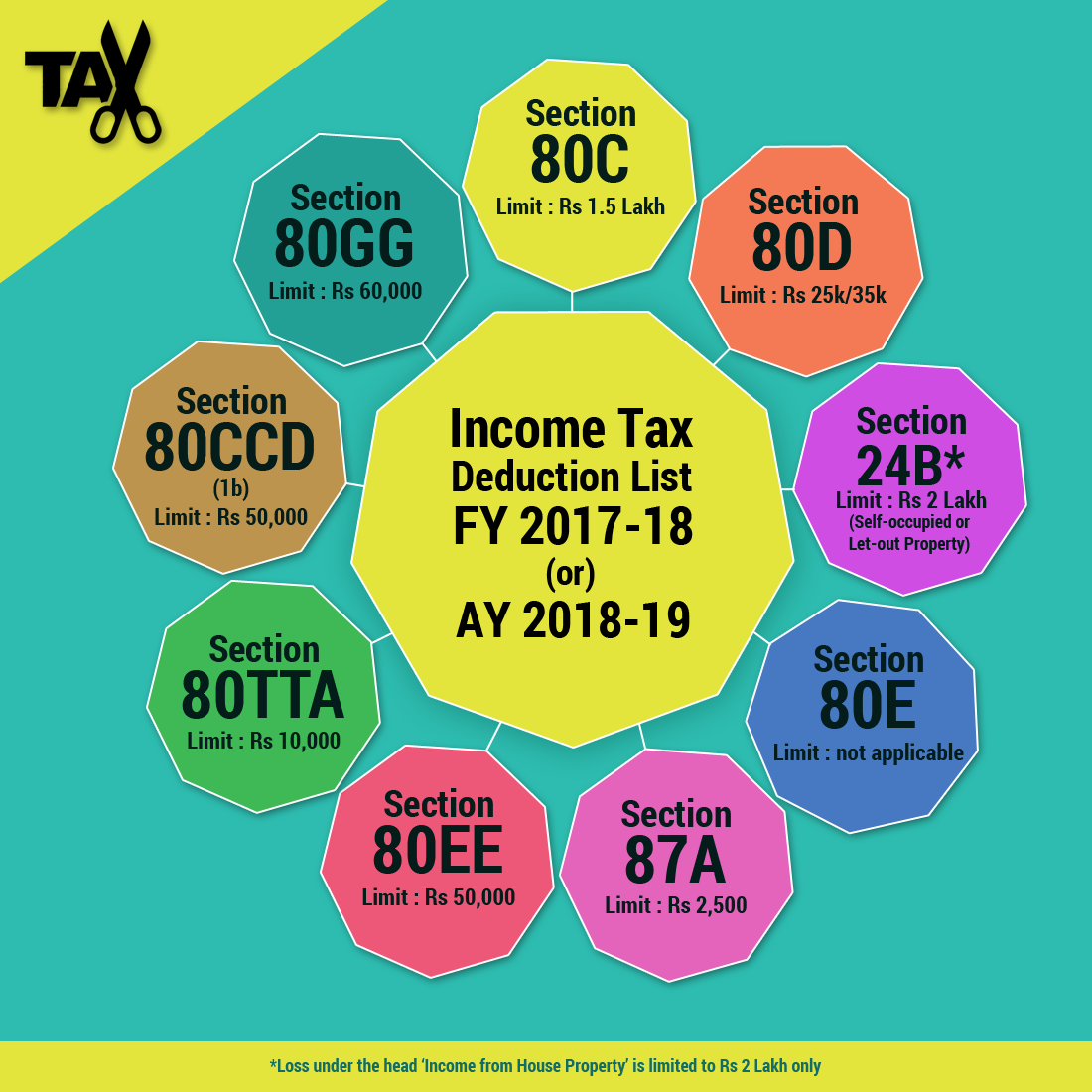

Let us unveil the list of Income Tax deductions under various Sections of the Income Tax Act,1961 for the Financial Year 2019-20.

Table Content

1. Section 80C

This is the most popular section under which taxpayers avail the tax deductions. The maximum tax exemption available under this section is Rs 1.5 Lakhs. One can claim for the tax deduction under this section for various expenses and investments done. You invest in one of the options or many the maximum deduction is capped to Rs 1.5 Lakhs only. There is a list of expenses and investment options under this section to claim tax deductions which are: Life Insurance Premium, Employee’s Provident Fund (EPF), Public Provident Fund (PF), National Pension Scheme (NPS), National Savings Certificate (NSC), Sukanya Samridhi Account, ELSS Mutual Funds, Bank Fixed Deposits, Home Loan Principal Repayment, Children’s Tuition Fees, Post Office Time Deposit, etc.

Section 80CCC

Contributions for a pension plan offered by an insurance company is tax deductible under this section up to a maximum of Rs 1.5 lakh. This section is a subsection of Section 80C only.

Section 80CCD

This section provides tax deductions for making contributions to the pension schemes offered by central government, including National Pension Scheme (NPS) and Atal Pension Yojana (APY). For salaried person, one can contribute 10% of the salary limit of the employee (80 CCD1) and additional tax benefit of Rs 50,000 u/s 80CCD (1b). A self-employed person can contribute 20% of his gross income (80 CCD1) towards government recognized pension schemes like NPS, Atal Pension Yojna.

The total deduction under section 80C, 80CCC and 80CCD(1) together cannot exceed Rs 1.5 lakh during FY 2019-20.

2. Section 80 D

Tax deduction is available for the payment of health insurance premium up to Rs 25,000 for self, spouse and dependent kids. If the individual or spouse is more than 60 years of age, the tax deduction limit has been increased to Rs 50,000 (previously it was Rs 30,000). Over and above this, an additional deduction for the payment of health insurance premium for the parents is Rs 25,000 (if the parents are below 60 years of age) or Rs 50,000 (if the parents are above 60 years of age). Within the specified tax deduction limits (as per age) one can also claim a deduction of Rs 5,000 for a preventive health check-up for self, spouse, dependent kids and parents.

3. Section 80 DD

Expenditure incurred on medical treatment of handicapped dependent relative is eligible for the tax deduction based on the degree of disability. In case where the disability is 40% or more but less than 80%, fixed deduction of Rs 75,000 can be claimed and for the disability, 80% or more, a fixed deduction of Rs 1,25,000 can be claimed. However, a certificate of disability (Form 10 no. 10-IA) is essential issued by the registered medical practitioner.

4. Section 80 DDB

Medical expenses incurred for specified critical diseases (mentioned in Rule 11DD) on self or family is eligible for tax deduction up to Rs 40,000 or actual expenses (whichever is less). For senior citizen & very senior citizen, the tax deduction can be claimed up to Rs 1,00,000 from FY 2018-19 onwards.

5. Section 80 E

Interest payable on the education loan taken for higher studies is eligible for the tax deduction for a period of 8 years or till the time interest is payable (whichever is lesser). There is no limit on the amount of interest paid specified for the tax deduction under this section. The education loan interest is eligible to offer tax benefits if taken for the tax payer himself, spouse, his/her kids or for someone for whom the tax payer is the legal guardian. There is no tax deduction for the repayment of the principal amount.

6. Section 80 EE

The deduction under this section can be availed by the individual first time house owners on the home loan sanctioned between 01-04-2016 to 31-03-2017. The property cost must be more than 50 Lakhs and the loan amount must be less than 35 lakhs. This deduction is not available for the running FY 2017-18. However, if you have claimed the tax deduction under this section in the financial year 2016-17, then you may continue to claim this deduction till the loan is repaid.

7. Section 80 G

Under this section the deductions can be availed on various donations disbursed for the social causes. The deduction eligibility is up to either 100% or 50% as per the qualifying limit with or without restrictions. With restriction the deduction is generally availed 100% or 50% deduction subject to 10% of adjusted gross total income based on the type of donation. Earlier, donations with an amount over Rs 10,000 in the form of cash was not eligible for the tax benefit under section 80 G. From the financial year 2017-18, the donation amount in cash with an amount of Rs 2,000 is not eligible to avail the tax deduction. The donation amount greater than Rs 2,000 is eligible for the deduction only if it is done in any mode other than cash like demand draft, cheque, etc.

- Some of the donations with a 100% tax deduction without any restriction are Prime Minister’s National Relief Fund, National Foundation for Communal Harmony, National Defence Fund set up by the Central Government, National Sports Fund, etc.

- Some of the donations with a 50% tax deduction without any restriction are Jawaharlal Nehru Memorial Fund, Prime Minister’s Drought Relief Fund, Indira Gandhi Memorial Trust, The Rajiv Gandhi Foundation.

- Some of the donations which are eligible for 50% deduction subject to 10% of adjusted gross total income are donations to any other fund or any institution which satisfies conditions mentioned in Section 80G(5), for repairs or renovation of any notified temple, mosque, gurudwara, church or other place, etc.

8. Section 80 GG

Under this section, the deduction is applicable when rent is paid and HRA is not received. The taxpayer should not have self-occupied residential property in any other place. The taxpayer, spouse or minor child should not own residential accommodation at the place of employment. Deduction available is the minimum of:

- Rent paid minus 10% of total income

- Rs 5000/- per month

- 25% of total income

For the financial year 2016-17 – Deduction calculation has been raised to Rs 5,000 a month from Rs 2,000 per month. Therefore a maximum of Rs 60,000 per annum can be claimed as a deduction.

Section 80 GGB

Contribution (as per section 293A of the Companies Act, 1956) made by an Indian company towards a political party (which is registered under section 29A of the Representation of the People Act) qualifies for tax deductions. Deduction is qualified only if the contribution is done other than cash.

Section 80 GGC

Contribution (as per section 293A of the Companies Act, 1956) made by an Indian taxpayer towards a political party (which is registered under section 29A of the Representation of the People Act) qualifies for tax deductions. Deduction is qualified only if the contribution is done by any means other than cash.

9. Section 80 RRB

The tax deduction under this section is related to the income earned on account of “Royalty of a Patent”.The deduction allowed is lower of Rs 3 Lakh or the actual income earned. The taxpayer must be an individual patentee resident of India.

10. Section 80 CCG

The deduction under this section is an account of Rajiv Gandhi Equity Saving Scheme, which was announced after the 2012 budget. Investors with gross total income of less than 12 Lakh can invest in the scheme and avail tax deduction, lower of 50% of the amount invested in equity or Rs 25,000 for three consecutive years. However, the scheme has been discontinued w.e.f 1st April, 2017. People who have invested in FY 2016-17 (AY 2017-18), can claim deduction under Section 80CCG until FY 2018-19 (AY 2019-20.)

11. Section 24

Tax benefit on loan repayment of second house will be restricted to Rs 2 lakh per annum only (even if you have multiple house the limit is still going to be Rs 2 Lakh only and the ceiling limit is not per house property). The unclaimed loss if any will be carried forward to be set off against house property income of the subsequent 8 years. In most of the cases, this can be treated as ‘dead loss‘.

12. Section 80 TTA

Under this section deduction up to a maximum of Rs. 10,000/-, in respect of interest on deposits in savings account with a bank, co-operative society or post office from the gross total income of an individual or HUF, can be claimed. Section 80TTA deduction is not available on interest income from fixed deposits.

13. Section 80U

This is similar to Section 80DD. Tax deduction is allowed for the tax assessee who is physically and mentally challenged.

Final Word

It is imperative to do the tax planning at the beginning of the financial year and avoid it to keep it for the last moment. It is important to plan your taxes based on your financial goals. Avoid investing in multiple investments rather it is important to analyze which one suits you the best. Understand various sections and analyze your deduction limits. Tax planning is not difficult if done timely with prudent investments.