How a Term Insurance Policy helps You Save Your Taxes?

When it comes to buying a tax-saving financial product, getting term life insurance coverage is the best bet. If you have dependents like spouses, children, and parents, it is extremely essential to have adequate life insurance coverage. When looking to ensure financial protection for your family, you may opt for a term insurance plan. It pays an amount equal to the sum assured (life cover) chosen, upon your unfortunate demise during the policy term and it is payable to the nominee, as opted by you under the policy.

| According to an online ‘protection survey’ conducted by Aditya Birla Sun Life Insurance, in the year 2017, 78% of people raise concerns over the uncertainty of life. At present, in metro cities, 83% of people feel uncertain about life and in non-metros, 67% of people feel uncertain about life. |

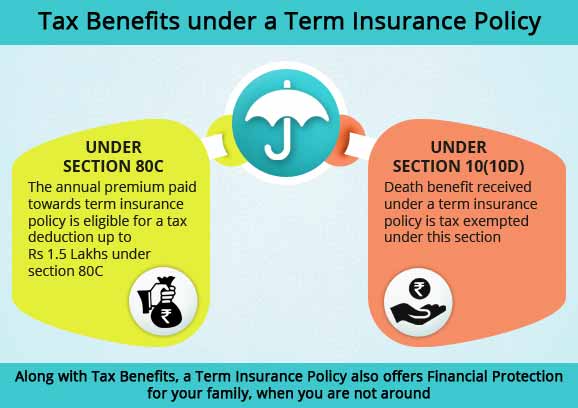

Considering the rising concerns over the risk of life, it’s quite essential to get them life coverage, so you don’t need to worry about the financial protection of your family against uncertainties. In addition to ensuring financial protection, a term insurance policy also offers tax benefits under sections 80C & 10(10D) of the Income Tax Act.

Table Content

- Tax Benefits Under Term Insurance Plan

- Under Section 80C

- Under Section 10 (10D)

- Ideal Life Cover You Need Under a Term Insurance Policy

- Household Expenses

- Inflation

- Education/Marriage Expenses of your Child

- Existing Liabilities

- Existing Investments/Savings Life Insurance Policies

- Cost of Term Insurance

- Bottom Line

- Related posts:

Tax Benefits Under Term Insurance Plan

A term plan also helps you in reducing your tax liability in the following manner.

It works like this:

- You buy a term insurance policy

- You pay the premium as per the coverage opted for and the policy term chosen as per your current age

- While calculating tax, the premium amount is reduced from your total income, thereby reducing your income and subsequent tax

- You can deduct a maximum of up to Rs 1.5 lakhs by buying a life insurance policy

- Your income reduces maximum up to Rs 1.5 lakhs in the eyes of the income tax authorities

- The tax will be calculated tax as a percentage of your income

- With the reduced income, your tax reduces too

- By buying life insurance of up to Rs 1.5 lakhs, you can save as much as 30% of Rs 1.5 lakhs which accounts to be Rs 45,000

Under Section 80C

The premium paid towards the term insurance policy is eligible for tax deduction under section 80C of the Income Tax Act, 1961. Individuals, as well as members of the Hindu Undivided Family (HUF), can enjoy the tax benefit under this section. For individuals, you can avail of the tax benefit in case the policy is taken in your life, your spouse, and/or dependent children’s life. For HUFs, any member of the family is eligible to avail of tax benefits.

Section 80C provides a tax deduction for the annual premium paid towards a term insurance policy up to Rs 1.5 lakhs. However, there are certain clauses related to the tax deduction, which are helpful to understand how the deduction can be availed.

- For the policies issued on or after 1st April 2012, the tax deduction can be availed if the annual premium payable does not exceed 10% of the sum assured. For policies issued on or prior to 31st March 2012, the total annual premium limit was up to 20% of the sum assured, to be eligible to avail of the tax deduction.

- If you are suffering from any illness or disability, the tax deduction is applicable when the paid premium is limited to 15% of the total sum assured. This clause is applicable to policies issued on or after 1st April 2013.

Under Section 10 (10D)

Death benefit received under a term insurance policy is tax exempted under section 10(10D) of the Income Tax Act, 1961.

However, this tax exemption clause would not be applicable under the following circumstances.

- Amount received under Section 80DD (3), (deposit made for maintenance, including medical treatment of handicapped dependent).

- If a policy is issued on or after 1st April 2003 but on or before 31st March 2012, any amount is received except death benefit. The tax exemption will also not be applicable if the annual premium paid is exceeding 20% of the sum assured.

- If a policy is issued on or after 1st April 2012, the tax exemption will not be applicable, if the annual premium paid is exceeding 10% of the sum assured.

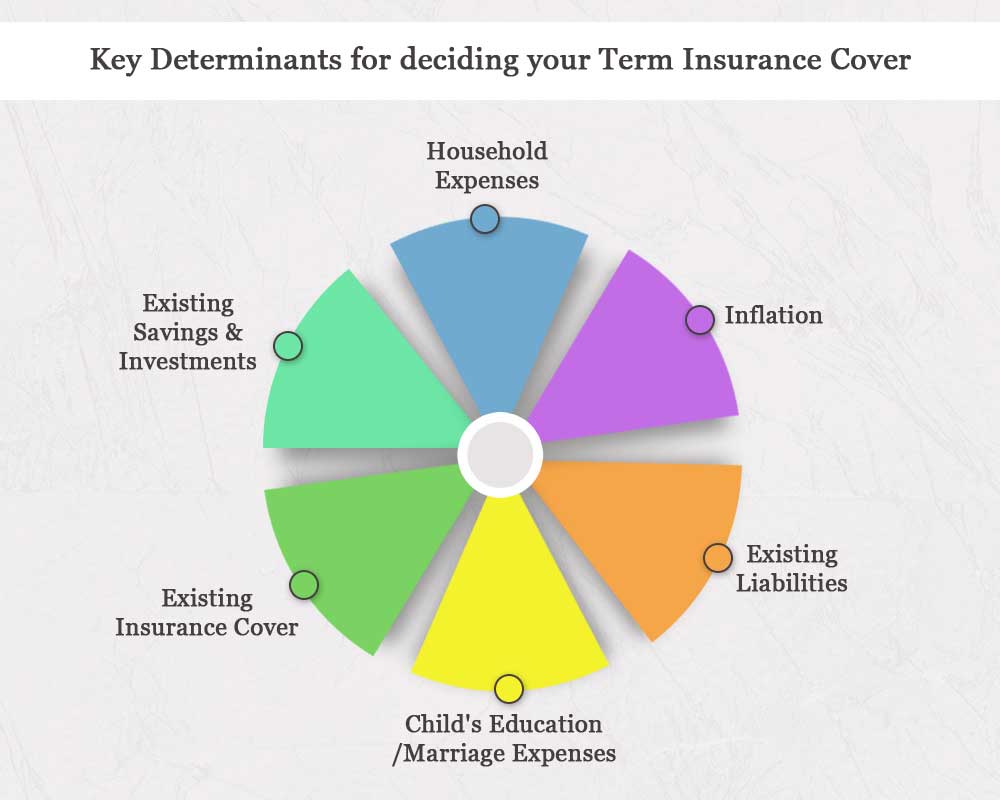

Ideal Life Cover You Need Under a Term Insurance Policy

You want to buy a term insurance plan but are not sure how to choose the right life cover (sum assured) which can fulfill your family’s financial needs when you are not around. Being underinsured (buying a lesser sum assured as required) will leave your family with a shortfall of finances, and being overinsured will only increase the cost (higher annual premium for a higher sum assured). The need for financial cover has been always different for different people and it is thus essential to assess your exact requirement of the sum assured.

There are some key factors that are accountable for determining the life cover you exactly need.

Household Expenses

Take an estimate of your present monthly household expenses you incur such as recurring living expenses, monthly rent, paying for utilities (electricity, water, gas refill), and other variable expenses, including the amount you spend on groceries, shopping, rationing, outings, etc. each month.

Inflation

Don’t forget to consider inflation, when it comes to computing monthly expenses. Expenses such as household expenses, housing & accommodation, entertainment & traveling, personal goods, clothes, etc. are inflationary expenses. Inflation is quite sensitive, if it increases or decreases marginally, the need for your life cover will change drastically.

Education/Marriage Expenses of your Child

Considering the present age of your child is 1 year and you want to accumulate the amount, so he/she can go for an engineering course at 20 years of age. To make your child’s dreams come true, you need to save around Rs 25 lakhs – 30 lakhs to meet the education cost of your child. Marriage expenses are also rising which could account for Rs 25 Lakhs to any amount as per the budget. In the event of your untimely demise, the right and adequate amount of sum assured will help to sponsor the education and/or marriage funds for the child.

Existing Liabilities

Existing liabilities would imply that you need to add all your outstanding loans. If, you had taken a home loan of Rs 25 lakhs, 2 years ago and the principal amount of 24 lakhs is still outstanding. Add up other loans such as auto loans, personal loans,s and credit card balances. If you had taken the entire loan amount of Rs 30 lakh, so consider this amount while computing the life cover. In the event of your demise, your family will not have the burden to pay it off, as the proceeds from the term insurance plan will be helpful to get rid of the outstanding loans if any.

Existing Investments/Savings Life Insurance Policies

Add up financial assets such as bank balance, fixed deposit, recurring deposit, government bonds and shares, mutual fund investment, and stocks trading. Take the total count of all your investments made. The current value of investments will be considered as savings and you may subtract it from liabilities while computing the term insurance coverage. If you have already taken life insurance policies and still continuing with it, you need to add up the life cover (sum assured) of all policies which would further help in assessing the right sum assured.

Let us understand it with an example:

| Rahul, who is 30 years of age, is a software engineer living with his spouse (non-working) and one child aged 1 year. His annual income is 10 Lakhs. He incurs monthly household expenses of around Rs 30,000. If considering an average rate of inflation of @10% with Rahul’s current monthly expenses of Rs 30,000, he will need to accumulate a corpus amount of Rs 62,81,785 to meet his family’s monthly household expenses for the next 30 years (till he attains age 60). The total household expenses are calculated till he reaches 60 years, as up to this age Rahul’s child will be independent financially. |

| Determinants of an Ideal Term Insurance Cover | Ideal Term Insurance Sum Assured for Rahul |

|---|---|

| Approximate household expenses for the next 30 years, including 10% inflation -A | Rs 63 lakhs |

| Education Expense of his child- B | Rs 30 lakhs |

| Existing Liabilities -C | Rs 22 lakhs |

| Existing Life Insurance coverage-D | Rs 10 lakhs |

| Accumulated Savings-E | Rs 5 lakhs |

| Ideal Term Insurance Sum Assured | A+B+C-D-E= (63 +30 + 22 -10 -5) Lakhs = Rs 1 crore |

Cost of Term Insurance

Term Insurance premiums are the most cost-effective because of the fact that the term insurance plan is a pure life insurance product. It implies that the term insurance plan only offers a death benefit and if the person survives the policy term, no maturity benefit is payable under a pure term plan. Since there is no maturity benefit that an insurance company is bound to pay, the premium of a term plan consists of a price to cover death and administrative expenses only. So, for opting for a high sum assured at a younger age, the premium is cheap and affordable.

| Rahul who is a non-smoker at 30 years of age buys a term life insurance policy of Rs 1 crore. For getting this life cover, he needs to pay the premium of Rs 7,497 per annum for a 30-year policy tenure. Per day cost to avail a sum assured of Rs 1 crore cover till the age of 60 is just Rs 20.54 which makes it evident that a Term Insurance Policy is quite affordable to ensure comprehensive financial protection for the family. Note:-The premium of a term plan may differ from one insurer to another. The premium payable may also increase if the tenure of the term policy increases. |

Bottom Line

A term insurance plan offers comprehensive financial protection for your family, in case something unfortunate happens to you during the policy term. You only need to thoroughly assess the financial requirement of your family and choose an adequate life cover, which will take care of your family’s standard of living and help to meet financial obligations, when you are not around.

Apart from providing a life cover, a term plan also ensures tax benefits under the Income Tax Act, 1961. You can avail tax benefits under section 80C for the premiums paid & under section 10(10D) for the policy benefits received. So, plan wisely you’re investments to reduce your tax liability and ensure a dual benefit of financial protection with a Term Insurance Plan.

I have taken ICICI Pru iProtect Smart term insurance plan with life option (no rider of acciedntal death benefit where double of sum assured is given).

In the policy document it is written that “We will pay the Death Benefit (DB) to your nominee, on the Death of the Life Assured”

it is also written that “Accidental Death Benefit (Rs.): NA”. Nowhere it is written that it is just a rider.

They are not willing to modify the rider comment as “Accidental Death Benefit (Rs.): Sum assured only”

One of my friend told that they can deny the sum assured in case of accidental death as it is written not applicable. sum assured will be given in case of natural death only. Is it the correct interpretation?