Bank Fixed Deposit to serve as a Tax Saving Tool

Fixed deposit is a financial instrument offered by banks or NBFCs, which allows investors to earn higher interest rates than a savings account. It is one of the most-popular investment options, as it offers the safety of your investments along with guaranteed returns. The tenure of Fixed deposits (FDs) may vary from 7 days to 10 years.

Table Content

Tax Saver Fixed Deposit

As the financial year is coming to an end, people are mostly looking for an investment option that can facilitate them to save tax. When it comes to fixed deposits, tax saver fixed deposit will help you to reduce the tax liability. A fixed deposit that comes with a maturity of at least 5 years or more is classified as a “tax saver fixed deposit “and it is eligible to avail tax benefits as well. These FDs however, don’t offer premature withdrawals and it gets locked throughout its tenure.

Reasons to Choose Tax Saver FD’s

- A Tax Saver Fixed Deposit enables you to get a tax deduction on your invested money up to Rs 1.5 lakhs under section 80C.

- The principal payment at maturity is tax exempted.

- It comes with a fixed interest rate that ensures guaranteed returns.

- You have the flexibility to choose a nominee, who can withdraw the amount in the event of your death.

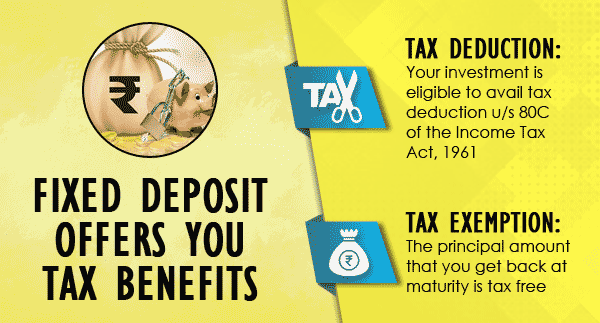

Tax Benefits

By investing in a tax saver FD, you are not only entitled to receive a fixed amount at maturity, you can also get the tax benefits.

Tax Deduction

The amount invested in a tax-saving fixed deposit scheme is eligible for a tax deduction up to a maximum of Rs 1.5 lakhs under section 80C of the Income Tax Act, 1961. In case of joint holders, only the first holder can avail the tax deduction. The amount invested can then be deducted from the gross total income to compute the taxable income during a financial year.

Tax Exemption

The principal amount that you receive at maturity is tax free. However, the interest earned is fully taxable. The interest income is added to your total income and taxed as per the slab rate applicable to your total income.

You have the option to receive the interest payout on monthly/quarterly basis or can be reinvested as well. The TDS will be deducted only when interest income (interest payable/reinvested) per customer across all branches, exceeds Rs 10,000 during a financial year. You can also avoid TDS deduction by submitting Form 15G (or Form 15H for senior citizens) to the bank.

Usually, TDS is deducted at a rate of 10% of the interest income. However, it will be levied @20% if you don’t provide PAN information to the bank. The fixed deposit receipt as issued by the bank shall serve as an investment proof for claiming tax benefit.

Types of Tax Saver Fixed Deposits

The tax saver fixed deposits can be held in either Single or Joint mode.

- Single holder type FD: This type of deposit shall be issued to an individual for himself/herself. In case of HUF, it is issued to the head (karta) of the family.

- Joint holder type FD: This type of deposit is issued jointly to two adults or to an adult and a minor.

Who can Invest?

- Only the Individual Indian Residents and members of Hindu Undivided Family (HUF) can invest in tax saving fixed deposit scheme. A minor is also eligible to get a tax saving FD jointly with an adult. Senior citizens (aged 60 years & above) and NRIs are also allowed to invest in this fixed deposit scheme.

- You can can invest in these fixed deposits by approaching to any public or private sector bank, except co-operative and rural banks.

Interest Rates

The interest rate under a tax saver FD differs, depending on the bank chosen, duration and amount of investment. Most of the banks offer slightly higher interest rates, usually 0.50% to senior citizens.

Interest Rates Offered by Top Banks

| Bank Name | Deposits (<1 crore) | Deposits (= or > 1 crore) | ||

|---|---|---|---|---|

| Interest Rate (per annum) | Senior Citizen Rates | Interest Rate (per annum) | Senior Citizen Rates | |

| SBI | 6% | 6.5% | 5.25% | 5.75% |

| PNB | 6.25% | 6.75% | 6.25% | 6.75% |

| Axis Bank | 6.25% | 6.75% | 6.25% | 6.75% |

| ICICI Bank | 6.55% | 6.55% | 6.55% | 6.55% |

| HDFC Bank | 6% | 6.5% | 4.85% | 5.35% |

Note: The interest rate mentioned in above table is for tenure of 5 to 10 years.

Investment Limit

The minimum deposit amount that you can start investing is Rs 100 and it may vary from one bank to another. The maximum amount of investment during a financial year in a tax saver fixed deposit is Rs 1.5 lakhs.

Nomination

Nomination facility is available for the tax saver FDs. You can choose a nominee under this type of the fixed deposit. You need to fill a form as prescribed under the Banking Companies (Nomination Rules), 1985. In case of your death before maturity of the fixed deposit, the appointed nominee or legal heir can withdraw the money from Tax saving FDs.

Transfer

You have the flexibility to transfer a tax-saving FD from one bank branch to another. You only need to apply at either of the two branches regarding transfer of your FD account.

Concluding Words

A fixed deposit scheme ensures a risk-free investment along with a fixed rate of interest which enables you to get the guaranteed returns. It is always advisable to go with a tax saver fixed deposit scheme that not only helps you to draw a guaranteed maturity value, it also offers tax savings. By investing in a tax saver fixed deposits, you can also avail tax deduction up to Rs 1.5 lakhs under section 80C of the Income Tax Act. The maturity value except interest earned is tax free.

Great blog about bank fixed deposit to serve as a tax saving tool was very helpful and informative thanks for such a great blog looking forward to read more of your future blogs.