How can You Save Tax by Investing in a Child Insurance Plan?

Being a parent, you always want to ensure a bright future for your child. When it comes to key milestones in the child’s life, such as higher education, marriage, etc. you don’t like to fall short on, at least on the financial front. Providing quality education is the key, as it helps your child to fulfill his/her dreams by investing in child insurance plan. However, the cost of education is increasing with every passing year and imparting education to your child has become a costly affair. The rising cost of education is the biggest worry among parents, as they are finding difficult to meet the child’s education needs.

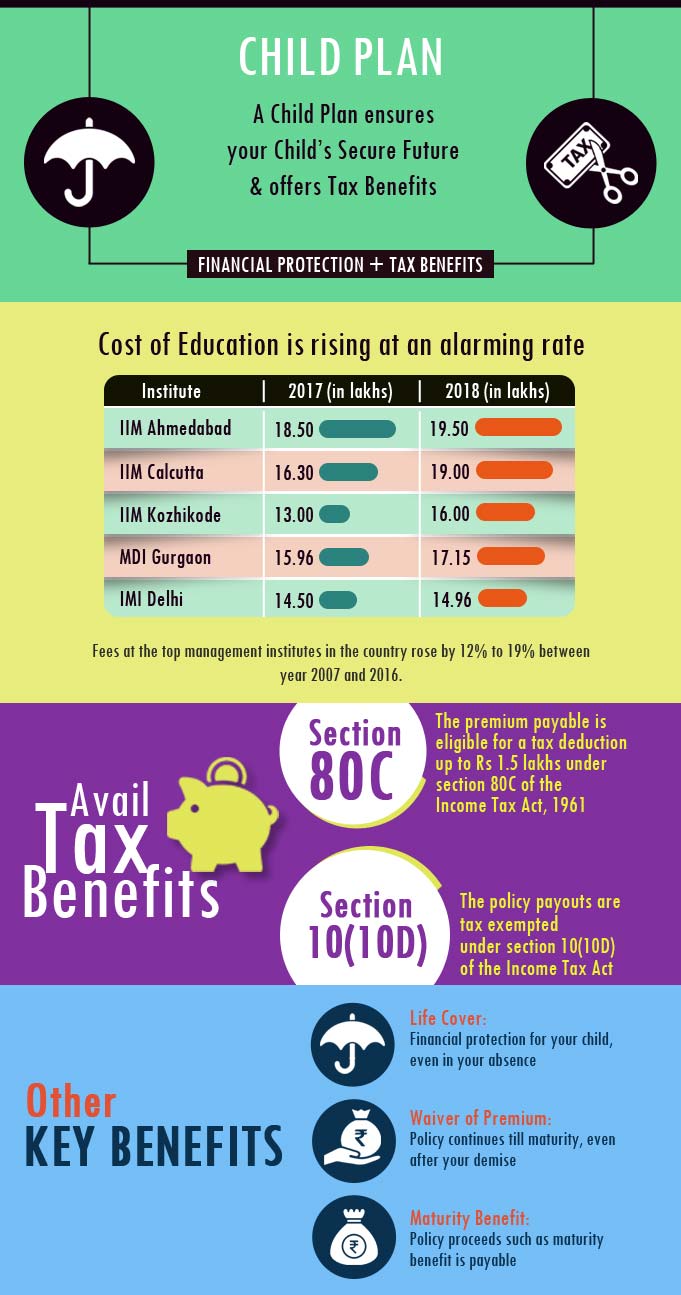

Table Content

Some Facts and Figures

Let’s go through some facts and figures focussing on the significance of robust financial planning to secure your child’s future.

|

If not planned prudently, you could fall short of the required corpus to give your children the best education and career ahead. The sharp rise in the education fees is a wake-up call for parents who still do not have a financial plan in place to combat the rising education cost. To fulfill the dreams and aspirations of your child, you need to have a disciplined saving for the secured future of the child. Investing in a CHILD INSURANCE PLAN ensures a safe future for your child and is one of the prudent ways to accumulate a corpus for them.

Child Plan- How It Secures Your Child’s Future?

Investing in child insurance plan ensures to build a corpus which can be used to secure a bright future for your child. It provides financial support to make your child achieve his dreams, even when you are not around. A child plan offers a lump sum payment on the untimely demise of the parent as well as future premiums are waived off, and the policy continues till maturity with the core purpose.

A child plan is a customized solution offered to parents aimed towards securing their child’s future.

Benefits under a Child Insurance Plan:

- Risk Cover: Investing in Child insurance plan offers a death benefit where the nominee gets the sum assured as a guaranteed amount, in case of death of the parent (who is the insured under the policy) during the term of the policy. The death benefit payable is really helpful for a child or the family to meet their financial needs, and the child does not have to compromise on the dreams and aspirations, the child wants to achieve.

- Waiver of Premium: Upon the death of the parent, a child plan does not terminate. The insurer offers a waiver of premium benefit where all the future premium payments are waived, and the policy continues till the maturity of the policy.

- Periodic Payouts: Most of the child insurance plans offer periodic payout at the milestone age of your child acting as a financial assistance to cater to the current need.

- Maturity Benefit: The maturity benefit, bonuses (if applicable) or other benefits as specified are payable. The lump sum amount payable at maturity can be utilized to fulfill the child’s future needs such as higher education, marriage expenses, etc.

A child plan thus ensures a comprehensive financial protection for your child and paves a way towards a bright future for the child.

Save Tax by Investing in a Child Plan

In addition to providing financial protection for your child, investing in a child plan also offers tax savings and helps you to reduce the tax liability.

Tax Deduction under Section 80C : The premium payable towards the child insurance plan during a financial year qualifies for the tax deduction under section 80C of the Income Tax Act, 1961. This tax deduction can be availed up to Rs 1.5 lakhs, while computing the taxable income.

Tax Exemption u/s 10 (10D) : The policy proceeds such as death benefit, maturity benefit, bonus (if any) under a child plan, not only offers financial assistance to your child, it also provides tax exemptions on policy payouts under section 10(10D) of the Income Tax Act.

Types of Child Insurance Plans

Traditional Child Insurance Plan: Traditional child plans carry the twin benefits of savings and insurance. On maturity, you are entitled to receive the sum assured plus the accrued bonus or guaranteed returns and on your premature death, the lumpsum amount is paid to your nominee who is a “child” under a child plan. For some plans, the child can be the life insured as well where parent being the policyholder. The traditional child plans offer safe returns on your invested premium amount to take care of the financial requirements for the child’s education.

Unit Linked Child Insurance Plan: Unit linked child plans are such plans which offer a dual benefit of “market linked investment” to build a corpus for your child’s educational needs and “ insurance” to stabilize your child’s future financially in the event of your unforeseen death. The unit linked child plan will allow you to build a decent corpus over a period of time to provide your child a secure and robust financial future.Unit Linked Child plans offer the flexibility and transparency in the investment in your hands. You may opt to put your money in equity (aggressive) or debt (conservative) related fund as per your risk capability. At maturity, the child ulip plan will give you a Fund Value which is the total amount of your invested fund. In the event of unfortunate death of the parent during the policy term, the unit linked child plan will provide Sum Assured or Fund Value, (whichever is higher) to the nominee.

Things to Ponder before Buying a Child Plan

- Evaluate the Required Funds: Before buying a child insurance plan, it is important to assess and calculate the funds to take care of the education needs and other extracurricular needs of your child.It is advisable to take into account the rate of inflation too.The amount can be easily calculated by using online calculators available on the insurer’s website.

| Suppose, the child’s current age is 1 year and you want a substantial corpus of Rs 20 lakhs when your child is about 21 years of age for his higher education. You need to save Rs 23646.77 monthly (amount calculated via HDFC Life child insurance plan calculator) for the policy term of 20 years to sponsor the higher education of your child. The funds required may differ depending on your child’s financial needs at key milestones. |

- Get Adequate Protection: Upon your unfortunate demise, the chosen sum assured will be payable to your nominee, which will help to cater the financial needs of the child.

- Choose an Ideal Policy Tenure: Determining the ideal tenure of the policy is a key factor. It will help you to accumulate an adequate amount to fulfill the financial needs at different milestone stages of the child.

Ideal tenure can be calculated as the child’s age at which you need funds less the current age of the child.

| If you decide to buy a child plan when your child’s age is 1 year and want to accumulate the required funds when your child is aged at 21 years. So, the ideal policy tenure is 20 years (21 years – 1 year). |

- In-built Waiver of Premium Benefit: When it comes to buying a child insurance plan, it is advisable to choose a plan which comes with in-built waiver of premium benefit. This benefit waives all the future premiums which ensures that the policy continues through the remaining tenure, if something unfortunate happened to you. With waiver of premium benefit, all the specified policy benefits such as maturity benefit, bonuses, etc., are payable.

- Compare Plans Online: Before buying a child plan, it would be a prudent move to compare various child insurance policies online. Comparing online helps you to check the benefits available, its exclusions,terms & conditions applicable.

Buying a comprehensive child plan is the best gift you can give to your child. It secures the future of your child, even in case of any eventuality. Investing in a child plan also allows you to avail tax benefits under section 80C & 10(10D) of the Income Tax Act, subject to prevailing tax laws.

Just Get One Baby One month before

I am poor I want save my amount for baby

Please contact

9379608346

In order to secure your child’s future, you may choose to buy ‘HDFC Life YoungStar Udaan’ plan that meets his/her academic expenses and other specific goals such as college fee, maariage expenses, etc.

I need to know a plan which yields 3 crores at end of 23 years

You can choose to buy HDFC SL YoungStar Super Premium Plan to secure the future of your child. You need to simply choose a sum assured amount to get the cover for your child and enter other personal details such as your age, your child’s age, etc to get the cover.